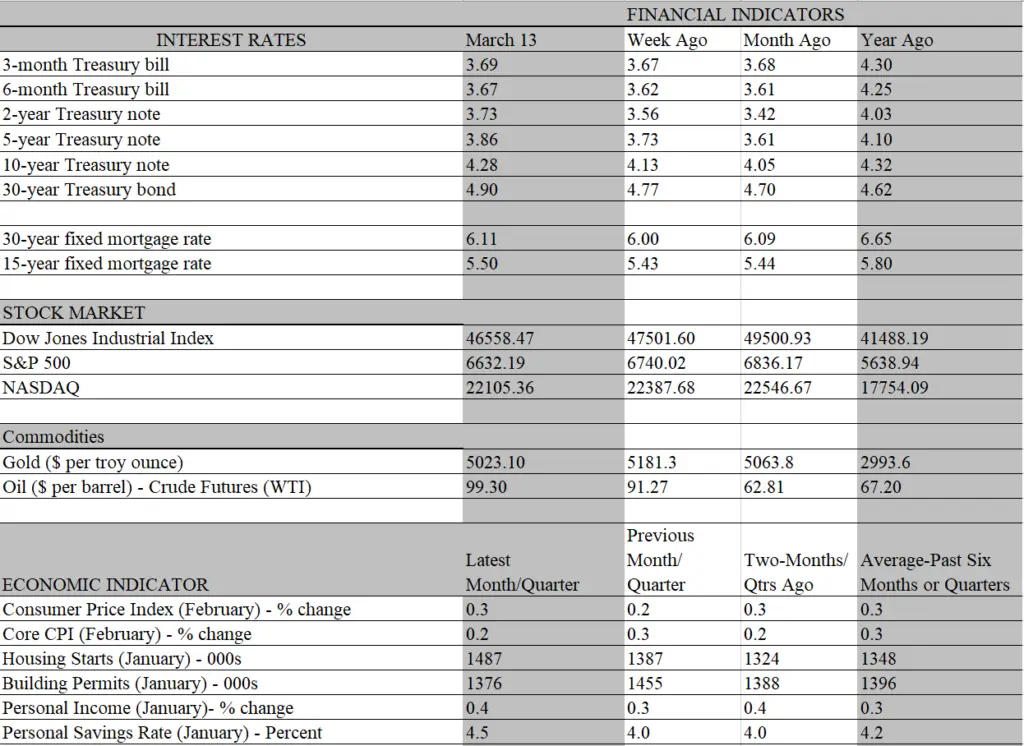

The fog of war is shrouding the economic outlook, and only time and the amount of devastation will determine the ultimate outcome. Aside from human lives, the oil market has so far been the primary victim of the Mid-East conflagration; but the energy sector’s tentacles reach far and wide and the longer tensions persist, the greater will be their effects. The surge in crude oil prices since the US/Israel attack on Iran and the closure of the Strait of Hormuz has been dramatic, briefly hitting $115/barrel before descending to the still-elevated $90-$100 range. Motorists are already feeling the pain, as pump prices are up almost 20 percent since the start of the war. The biggest hit to wallets will be felt by lower-income households, who spend more of their budgets on gasoline and other energy-related goods and services.

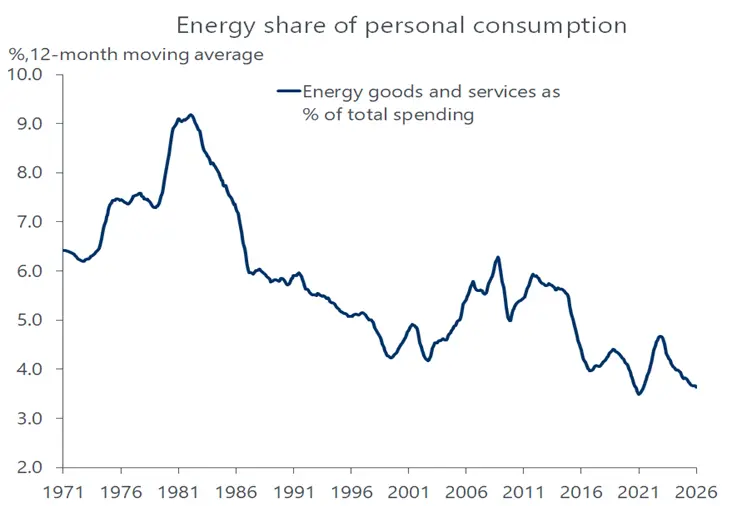

That said, surging energy prices should have more of a negative impact on headline inflation than on growth, at least over the short term. Comparisons with previous oil shocks, particularly with the 1970s when the Mid-East was also the catalyst of soaring gas prices and sending drivers on long lines at the pump, are irrelevant. Back then, the oil shock dealt a double whammy on the economy, as the gas “tax” on income stifled growth even as it stoked inflation. There will be a stagflationary impact this time as well, but milder and not as two-sided as it was then. One reason is that the economy, and particularly households. have become far less dependent on oil. Indeed, consumers devote less than half of their spending share on energy-related goods and services than they did 50 years ago. The economy as a whole, has become much less energy intensive than it was then.

But it would be a mistake to downplay the psychological impact of both the war and the highly visible price hikes on service station signboards is having on the public. Consumer sentiment has been in the dumps for some time, and the early March reading by the University of Michigan indicates that the sinking feeling continued even before the full impact of the war was captured in the survey. To be sure, consumer spending generally bears a loose relationship with sentiment, but when an external shock is added to the mix – and takes a real bite out of purchasing power – the link becomes tighter. Energy costs may not be as dominant in household budgets as before, but any additional expense amid widespread affordability concerns could have an amplified impact on spending.

The consensus view is that the war will not persist long enough to send the economy off the rails or drive inflation sustainably higher. We agree with that assessment and note that the pillars of growth remain mostly intact. Nor have inflationary expectations on Main Street become unanchored, something that the Federal Reserve closely monitors. However, the cumulative effect of tariffs and now oil prices is seeping into the financial markets, as bond yields have risen markedly since the war started, with the bellwether 10-year Treasury yield up by more than a quarter of a percent. That, in turn, has short-circuited the decline in mortgage yields that had been underway and helped make housing more affordable for first-time homebuyers. After dipping below the psychological 6 percent threshold for a brief one- week period in late February, mortgage rates have since rebounded to 6.11 percent in the latest week and is likely heading higher next week.

The good news is that the gas tax on households is being offset by the reduced taxes on incomes and the large refunds that are now hitting bank accounts, thanks to last year’s tax legislation. Together with solid real wage gains, that should sustain the economy’s momentum through the first quarter. The bad news is that the year started with less momentum than earlier thought, as the fourth quarter’s GDP growth rate was revised down to 0.7 percent from 1.4 percent. And while the government shutdown was a significant drag that will be recouped in the first quarter, the private sector turned out to be less vigorous as well. Real final sales to private domestic purchasers – mainly consumers and fixed investment spending by businesses – was revised down to 1.9 percent from 2.4 percent.

It’s early days, made earlier on the data calendar by delays from the government shutdown, but incoming reports for January and February indicate the economy is still chugging along in a relatively benign inflation environment that has yet to be upended by the gas shock. Importantly, consumer purchasing power continues to hold up, as the 4.4 percent year-over- year increase in personal income in January outpaced PCE inflation by more than 1 percent. However, a deeper dive into the data suggests a cautionary note, as about 40 percent of the income gain in January came from dividend payments.

This source of revenue is punching well above its weight, as it accounts for less than 10 percent of personal income. Since wealthier households own the majority of dividend-paying stocks, it’s likely they were the prime beneficiaries of January’s bump in income. It also may explain the 0.5 percent jump in the personal savings rate to 4.5 percent in January. On the surface, the savings buildup could be viewed as potential fuel for spending down the road, reflecting a precautionary buildup of households in uncertain times. But if the additional savings came mostly from dividends, it would mainly buffer the wealth cushion of upper-income households rather than enter the spending stream.

Still, wages staged another solid gain in January, echoing the blockbuster increase in jobs that month. It remains to be seen how much, if any, of that gain will be sliced by the job losses in February. An encouraging note for job seekers is that job openings unexpectedly rose in January, indicating that the demand for workers has not dried up and businesses are not ready to downsize headcount, which would lead to more layoffs. Importantly, job postings for the main driver of payroll gains, the healthcare sector, have been on the skids, pointing to a weaker contribution from this critical source of jobs. However, healthcare postings turned up in January, indicating that demand for these workers has stabilized and is still well above pre-pandemic levels. Still, January is a noisy month for a swath of economic data, as it is when businesses reset plans for the year, including staffing needs.

Nothing in the latest batch of reports should move the needle for the Fed at its policy meeting next week, when it is expected to hold rates steady. However, the ground is shifting among traders who see the fog of war posing more of a risk to inflation than to jobs. Prior to the conflict, they put high odds on the Fed to cut rates twice this year. As of Friday, the betting shifted dramatically, with the odds of no more than one cut put at about 80 percent. All eyes will be on the quarterly economic and financial projection of Fed officials, which will be released at the meeting, to see how well they align with shifting market sentiment.