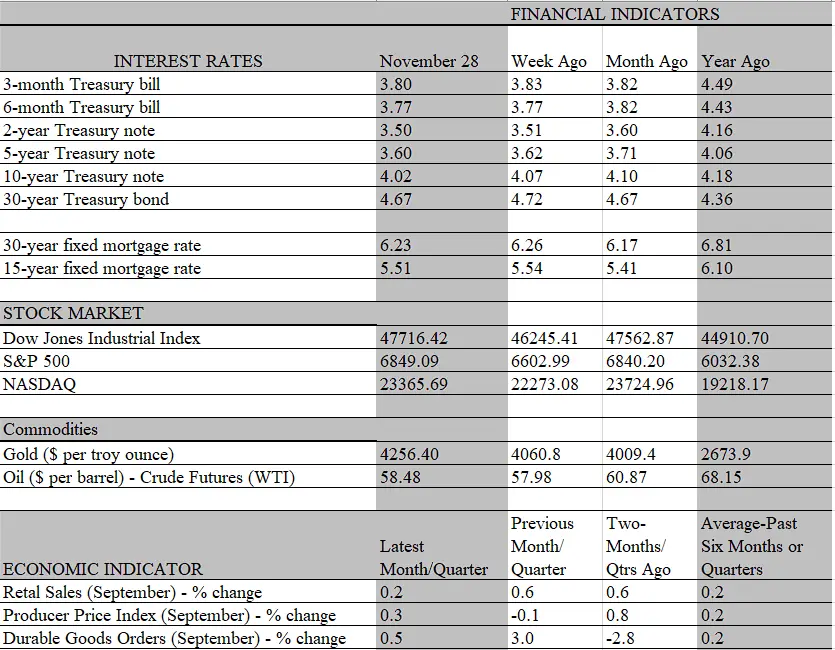

With the government reopened and the data mills humming once again, the health of the economy is gradually coming into better focus. Unfortunately, clarity is still elusive for what transpired in October and November, as only sketchy data for the former has been collected, and information for November is still being gathered. Hence, when the Federal Reserve meets to make its rate-setting decision on December 9-10, most of the data on hand will be stale. At this juncture, we still believe it is a coin toss whether it will cut again for the third time since September or stand pat. That said, the financial markets are pricing in more than a 70 percent chance that it will pull the rate-cutting trigger again, mainly based on recent dovish statements by Fed officials.

No doubt, the increased chance of a rate cut expected by traders is a primary influence stoking the stock market rally in recent weeks. But the debate over what the Fed does and what it should do has not been resolved and continues to elicit vocal supporters on both sides of the issue. The administration, of course, is a strong supporter of lower rates, something that is not unique with the current regime as incumbents traditionally prefer anything that adds vigor to the economy and the job market, even if it risks higher inflation – up to a point. True, pocketbook issues have been top of mind of voters, reinforced by surveys that indicate households are extremely agitated by high prices. But ask people if they would prefer lower prices on eggs or the loss of a job and the decision would be a no-brainer.

However, the Fed is supposed to take sentiment out of its decision-making process and formulate polices based on hard data. As noted, such evidence is in short supply these days, so private economists, investors and other interested parties are relying more on surveys and anecdotal information to gather information on the health of the economy. A key input for the Fed is the Beige Book, a survey of businesses in the 12 regional Federal Reserve districts taken every six weeks before the FOMC policy-making decision takes place. The information provided to committee members is more up to date than the hard data they have on hand even when the government is up and running; hence, it provides valuable secondary guidance on economic conditions. This time, the Beige Book may become more of a primary influence on how policy makers see the economy.

At first glance, the latest reporting from business contacts contained in the Beige Book, lends support to the doves on the Fed. Employment declined in the most recent six-week period, with about half of Districts pointing to weaker labor demand. However, the details matter, and the comments themselves about the labor market were probably not enough to convince the hawks on the Fed to support a rate cut in December. While the most recent Beige Book acknowledged the increase in layoff announcements, more Fed districts indicated that business contacts were curbing their headcounts, not through firings, but rather through hiring freezes, replacement-only hiring, and attrition. Also, firms are reportedly adjusting hours worked, instead of the number of employees, to better match their sales landscape. A few businesses cited AI displacing entry-level positions or making the existing workforce more productive, thereby reducing the need for new hiring. However, monetary policy won’t be able to address structural risks to the labor market from new technologies, so the AI influence on the Fed is not expected to be significant, if at all.

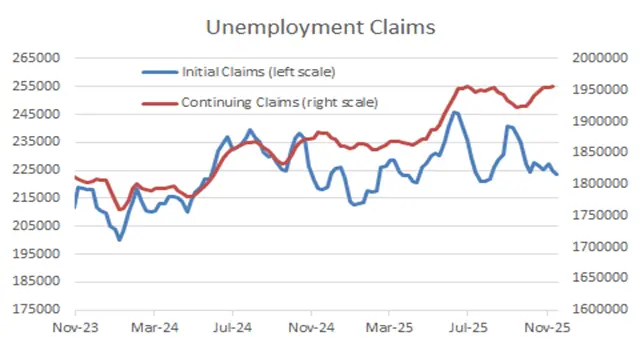

The comments by respondents regarding the staffing decisions is consistent with the low hiring/ low firing narrative that has been in effect for much of this year. That narrative was reaffirmed in the latest data on claims for unemployment benefits. New applications for jobless benefits continue to be relatively low, suggesting that companies are holding on to their workers. However, the number of people still receiving benefits, i.e., continuing claims, continued to rise steadily, climbing to a near four-year high. Simply put, with hiring put on hold, jobs seekers are having a hard time landing a position. On the surface, that no hiring/no firing combination may seem like a wash, but in reality it is a drag on the economy. Employed workers face stiffer competition from job seekers, which undercuts their bargaining power for wages, and heightens job insecurity, resulting to less spending than otherwise.

Elsewhere, some retailers indicated a negative impact on consumer spending due to the government shutdown. Community organizations witnessed greater demand for food assistance because of the disruptions to SNAP. Indeed, the tale of two consumers was evident in the Beige Book, which noted resilience in higher-end retail spending. Rising household wealth has supported consumption growth in an otherwise unfavorable backdrop, given the lackluster labor market, stubborn inflation, and heightened policy uncertainty. We estimate that every $1 in newfound wealth is associated with an additional $0.05 in consumption. Though the marginal propensity to consume out of wealth is low, the sheer amount of wealth generation has morphed into a key contributor to spending growth.

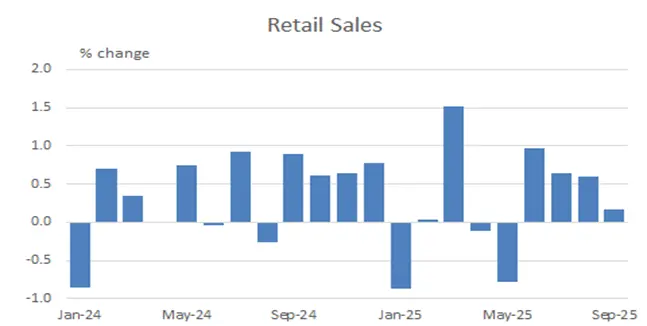

Again, the latest data we have for consumers is the retail sales report for September, released this week. While the report is stale and is not likely to significantly influence the Fed’s decision, it does reflect some of the forces evident in the Beige Book. Overall, retail sales came in softer than expected during that month, slipping by 0.2 percent compared to a consensus forecast of 0.3 %. But the setback comes after three months of robust gains and still punctuates a quarter of strong sales. Based on the data we have covering October and the first half of November, underlying spending still appears to be carrying plenty of momentum into the holiday shopping season.

Indeed, we expect the strongest holiday sales growth since 2021. While real incomes growth has slowed as tariffs have kept inflation elevated and slowed jobs growth, the strong gains in household wealth are helping to support spending, particularly from older and wealthier households. From our lens, the bifurcated consumer will continue to be a prominent feature heading into 2026. The labor market is likely to remain under pressure, in part because AI-related gains in productivity risk a jobless expansion in the coming years. Time will tell if the stock market continues to sustain the positive wealth effect on consumption for high-net-worth households. But the upper income cohort will be supported by the scheduled personal tax cuts, which will drive a stronger refund season next year. The tax cuts mostly benefit higher income households, particularly through the increased state and local tax deduction.