With the presidential and congressional races now settled, a key source of uncertainty has been resolved. Not so with the policy proposals or how they will be accepted by incoming legislators, much less the financial markets. Historically, bold campaign promises tend to be watered down before becoming reality. Despite gaining the popular vote and control of both chambers of Congress, presidents cannot ram through proposals deemed unacceptable by legislators whose constituents are not keen on what they contain. Even if President-elect Trump uses his executive power to raise tariffs, the ramifications would be highly uncertain depending on whether there is a tit-for-tat response by trading partners. Likewise, tax and spending proposals will navigate a complex landscape of public scrutiny over what should go and what stays.

Simply put, elections clarify who proposes, not who disposes or what proposals will eventually look like. On this score, those who believe that the prospect of higher tariffs, lower taxes, massive deportation, and deregulation should prompt the Fed to go slow in its easing campaign next year are barking up the wrong tree. Chair Powell correctly noted that it is far too soon to know what will come out of Washington in coming months, or what their impact might be. If nothing else, that uncertainty only reduces the odds of preemptive moves by the central bank, making it more reliant on backward looking data.

Indeed, in a speech in Dallas on Thursday, Powell noted that the economy is not sending signals that the Fed should be in a hurry to cut interest rates. Traders got the message and immediately dialed back the odds of a rate cut in December. We still believe the odds favor a reduction next month but also think the risk of fewer cuts in 2025 has increased. Keep in mind that there is still an important inflation and a jobs report scheduled for release prior to the mid-December FOMC meeting, which could have a major influence on the Feds decision. The jobs report will particularly come under the spotlight, as it will reveal how strongly the labor market recovered from the weather and strike -related losses in October. If the recovery delivered considerably more than just the catch-up of lost payrolls, the Fed could worry less about the emerging softness in job growth and pay more attention to inflation trends.

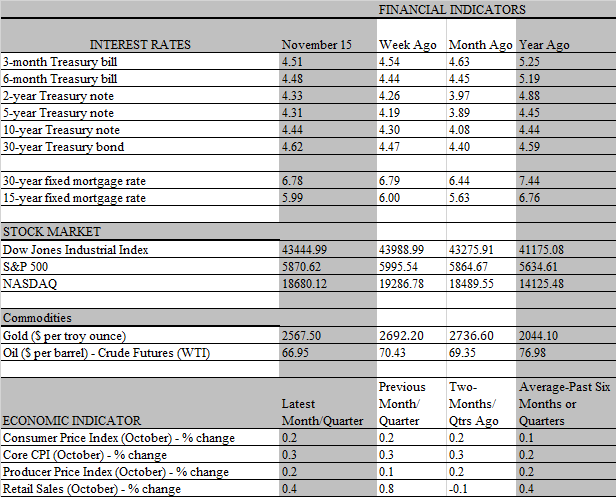

That may be a timely shift, as the latest inflation report supports the lack of urgency to cut rates. The headline consumer price index increased 2.6 percent from a year ago in October, up from 2.4 percent in September, marking the first acceleration since March. Base effects were the main culprit; the monthly increase stayed at 0.2 percent for the fourth consecutive month, but those steady increments translate into a climbing trend when measured against a steeply declining inflation rate in the second half of last year. Still, the headline acceleration is a stark reminder that the road to the Feds 2 percent inflation target will be riddled with potholes. Some stalwart impediments are slowing the journey, including elevated housing-related costs and service prices.

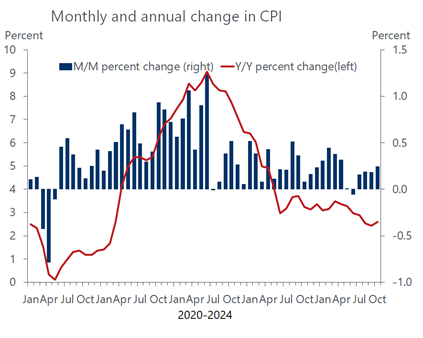

After an encouraging slowdown in September, shelter prices rebounded in October, increasing 0.4 percent. Compared to a year ago, shelter prices, including tenant rents and owners equivalent rent, increased just a tad under 5 percent. The Fed is probably not too concerned about this stickiness, as it still captures lease rollovers from a year ago into steeply higher rents. Market conditions have since changed, as current lease signings are seeing much smaller increases, in some regions, outright declines. More concerning is the stickiness in core service prices, excluding shelter, dubbed the super core inflation rate, which is increasing at an annual rate of 4.3 percent over the past three months. This grouping is heavily influenced by labor costs, suggesting the Fed would need to see more of an unwelcome softening in labor markets to curb wage growth. The good news is that stronger productivity growth enables employers to pay workers more without raising prices. The bad news is that the prospect of mass deportations portends cuts in the labor supply that puts upward pressure on wages.

These crosscurrents will complicate the Feds decisions heading into 2025. Adding to the muddy economic backdrop is the behavior of markets, driven by traders who may have a different perspective on conditions than the Fed. At this juncture, the rebound in market yields aligns with the less dovish sentiment expressed by Powell, with the 10-year Treasury yield hitting a five-month high on Friday, up more than three quarters of a percent since the Fed cut rates in mid-September. Whether or not this climb pressures the Fed to go more slowly in its rate-cutting campaign, it nonetheless acts as a brake on growth, delivering the equivalent of a stealth tightening of policy. In time-honored fashion, the housing sector will be among the first victim of the damage wrought by higher mortgage rates, which closely follows the Treasury yield. So far, the rise in mortgage rates has mainly stifled refinancing activity, which has been cut in half since mid-September, according to the MBAs refinancing index. But applications for home purchases have also turned softer.

The key for the broader economy will be whether the climb in market yields deters spending by consumers, the economys main growth driver. No doubt, the hit to home sales would deal a blow to a host of housing-related products and services, such as home furnishings, appliances and moving expenses. But households readily coped with elevating interest rates in 2022 and 2023, helped by generous stimulus checks and a strong job market that pumped up incomes. The fiscal largess has vanished, and the job market is softening; but consumers are still in good shape, thanks to healthy balance sheets for most Americans and cooling inflation that is bolstering real incomes. And while job growth is slowing, so too is the labor force as tighter border policies have reduced the flow of immigrants to fill positions. Hence, smaller payroll increases will not stoke a meaningful rise in unemployment nor stop wages from rising.

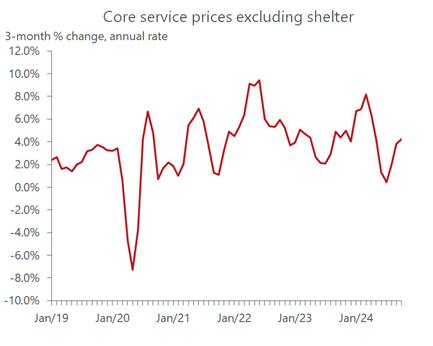

That households are still capable of keeping their wallets and purses open was confirmed in this weeks retail sales report. Not only did total sales stage a stronger gain in October than expected the increase in September was also revised sharply higher. Hence, the economy entered the fourth quarter riding more momentum than thought, giving heft to the growth rate over the closing months of the year. Similarly, the sharp upward revision to Septembers control group of sales, which feeds directly into personal consumption in the GDP calculation, more than offset its small decline in October. Significantly, the steep 1.3 percent decline in spending on home furnishings exceeded only by the 1.6 percent drop in miscellaneous store sales among the major categories may be an early signal of the impact that the climb in mortgage rates is having on the housing market.

That said, consumers are still flexing their spending muscles with few signs they are losing purchasing power. We expect personal spending will be a pillar of strength for the economy through the fourth quarter as well as next year. However, just as inflation retreated amid the robust growth rate over the second half of 2023, the disinflation trend should remain intact in 2025, allowing the Fed to continue gradually lower rates. Stronger productivity is boosting the economys potential growth rate, the labor market has come into better balance, taking the steam out of outsized wage increases, and inflation expectations have receded, settling close to the Feds 2 percent target. While the risk has increased that the Fed may slow the easing pace next year, rates are still highly restrictive. A softening job market and cooling inflation should further support the bias among officials to normalize policy as quickly as possible.