A widely admired principle states that when you’re surrounded by chaos, seek out the calmest person in the room for direction. That search is ongoing, but Fed chair Powell represented as good of a stand-in this week as anyone available. Given the heat coming from all sides, he was able to cobble together a consensus among policy colleagues under what most would consider impossible circumstances. Even before the Mideast war broke out, Powell was tasked with reconciling conflicting views regarding the impact of tariffs on growth and inflation, as both sides of the dual mandate remained deeply in tension. Add a raging war to the mix, one that only exacerbates that tension, and the challenge becomes even more daunting.

Yet the outcome of the latest policy meeting was greeted more with acceptance than derision, a palpable sign of success and a measure of Powell’s communication skills. Clearly, navigating an economy through multiple shocks in five years – a pandemic, two oil shocks, tariffs, an immigration crackdown and now a war – is no easy task. But the economy has remained afloat, and the Fed avoided knee jerk reactions that could have sent it off the rails. The meeting this week was no exception, even as officials were keenly aware of the high stakes from a miscalculation. To his credit, Powell readily acknowledges the mistake of waiting too long to snuff out the inflation flareup ignited in 2021, under the ill-fated belief that it would be transitory.

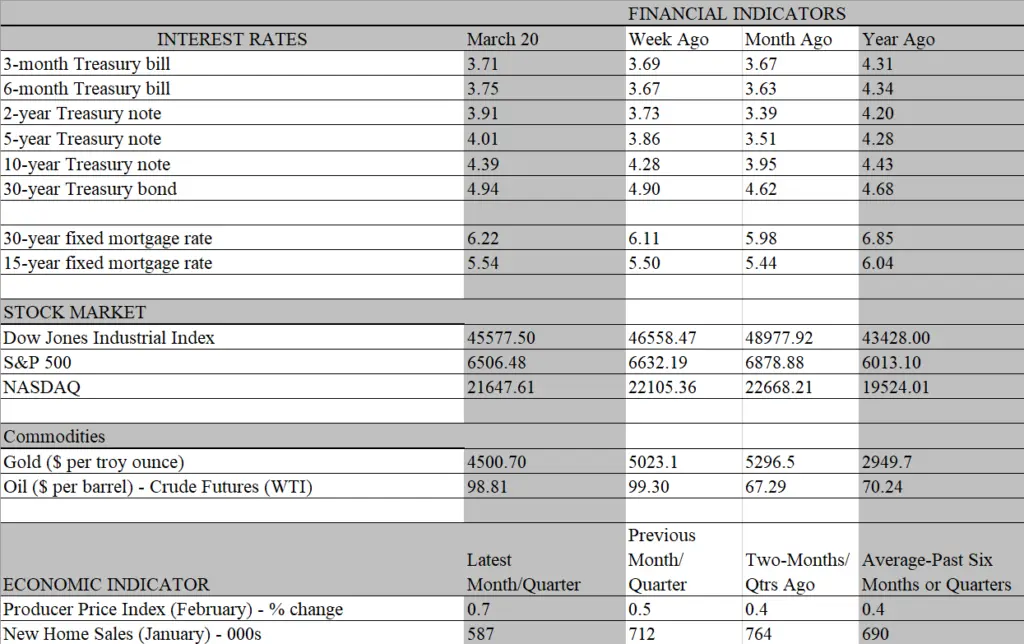

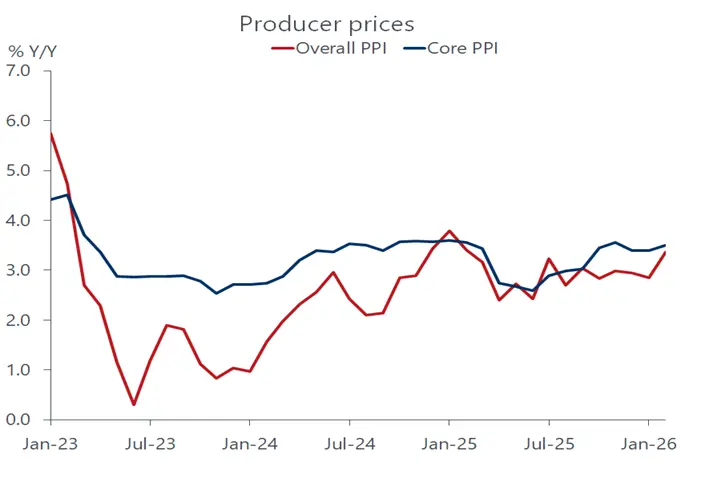

The decision at this week’s meeting to keep rates unchanged reflects, to some extent, a hangover from that episode. Despite growing signs of fragility in the job market – and persistent pressure from the White House – the Fed extended the pause in its rate-cutting campaign for the second consecutive meeting, citing uncertainty over what the Mideast war implies for the economy. While not explicitly noted in the policy statement or in the post-meeting press conference, Powell no doubt wants to avoid repeating the earlier mistake of letting inflation gain traction, this time from an oil-price spiral that becomes more embedded in the economy. It is highly unlikely that inflation will take off at anything like the speed and magnitude seen in 2022, but the second-round effects are becoming more visible, spreading to food, transportation and further down the pipeline, as evidenced by the strongest wholesale price increase in February since last summer.

To be sure, the decision to keep rates unchanged at the latest meeting was widely expected and should not be viewed as a hawkish turn in sentiment among Fed officials. As was the case in December, Fed officials still expect to cut rates before the end of the year, an implicit acknowledgement that inflation will recede once the Mideast war ends and the oil spigot reopens. We agree with that assessment and suspect the Fed may be underestimating the demand destruction caused by higher oil prices. Based on our own forecast of oil prices, we estimate that the increased cost of gasoline will wipe out the enhanced tax refunds hitting bank accounts, which were expected to impart a substantial growth impetus over the first half of the year.

Beyond the near-term drag on the economy from higher energy costs, the Fed remains concerned over the ongoing fragility in the job market that began well before the Mideast war got underway. Only the shrinking supply of labor related to the immigration crackdown has prevented the hiring strike of employers from lifting the unemployment rate more than it has. Powell noted in the press conference that this no hiring/no firing environment represents an uncomfortable balance, suggesting it masks more weakness than strength. It is hard to wrap your head around the notion that a fully employed economy is sustainable amid zero job growth, which is estimated to be the breakeven rate to keep the unemployment rate steady.

It would seem that other forces besides fewer immigrants are suppressing the growth in jobs. No doubt, companies are striving to normalize their workforce following the over hiring that took place during the early stage of the pandemic recovery. The removal of bloat is mostly, if not completely, accomplished. With a leaner staff generating as much output as before, companies have enjoyed a sizeable productivity boost that, in turn, has resulted in lofty profits, providing support to the stock market. A big chunk of those profits is being funneled into AI software and datacenters, which should give another leg up to productivity growth in coming years. The jury is still out as to how that impacts the demand for workers, as reducing labor costs is a key incentive behind the outsized spending on productivity-enhancing capital equipment, structures and AI research.

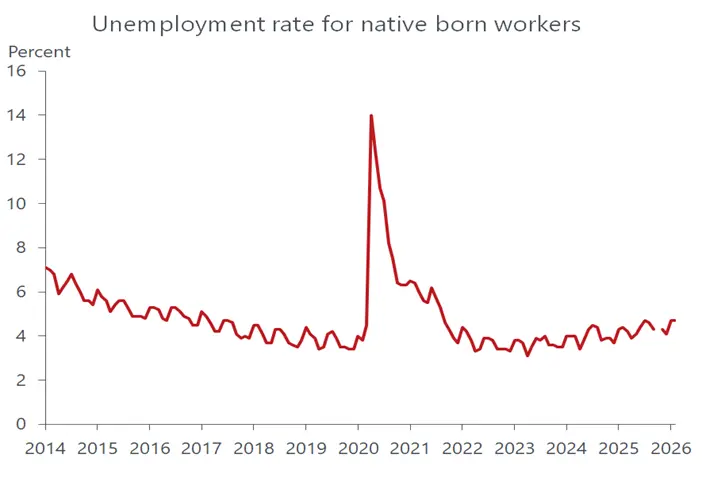

And while the supply constraint on the labor force from reduced immigration is clearly limiting the rise in the unemployment rate, it has not opened up vacancies for the native-born population. Indeed, the unemployment rate for native born workers stands at 4.7 percent, which is above the overall rate and matching the highest level since August 2021. If the demand for labor were the same as before the immigration crackdown, the unemployment rate for native born workers would be considerably lower, as companies would need to replace the lost immigrants. This points to another reason why the low overall unemployment rate is overstating the strength of the job market.

At this juncture, the oil-induced inflation flareup is grabbing most of the headlines, overshadowing its demand-destroying impact. However, the rise in energy costs is eating into disposable incomes and downside risks to consumer spending are growing. The most vulnerable consumers are those on the lower end of the income ladder who devote more of their budgets to utility bills and gasoline. That, in turn, portends a deepening of the bifurcated consumer experience this year. But the longer the Mideast conflict continues, the greater will be the risk to middle and upper-income households, whose spending is more heavily influenced by financial market conditions. So far, stock prices have not weakened enough to have a material impact on spending, but the direction of travel is decidedly down, punctuated by the just concluded fourth consecutive weekly loss in the S&P 500.

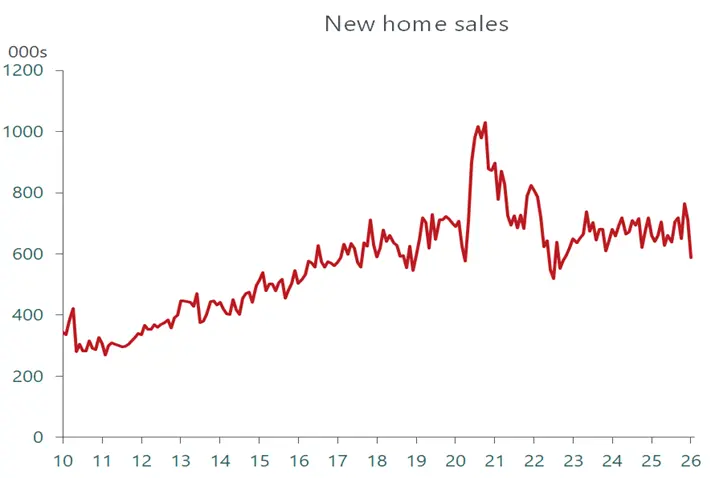

Meanwhile, market interest rates have been climbing, with the 10-year Treasury yield hitting the highest level since last July. That’s driving up mortgage rates and amplifying the affordability issue that is preventing a recovery in the moribund housing market. The plunge in new home sales in January reported this week was more in response to harsh weather conditions than mortgage rates, which were actually falling that month. Still, it boosted the supply of unsold homes, extending the time it will take for builders to clear inventories and start construction on new homes. With Treasury yields up by almost half-percent so far this month, the obstacle to home buying has only become stronger. We suspect that once the war is resolved, the downside risks to the economy will take precedence over inflation in the eyes of the Fed and open the door for rate cuts. From our lens, the Fed’s effort to short-circuit a major deterioration in labor conditions will require two rate cuts this year instead of the one currently projected at the latest meeting.