The first rate move under the last six Fed Chairs was an increase. You would have to go back to 1970 when the new Chairman, Arthur Burns, put through a rate cut under pressure from President Nixon. Will the latest newbie at the helm depart from the long list of his predecessors and oversee a rate cut? That question seemed almost unimaginable a few weeks ago when the prevailing sentiment at the Fed was tilting decisively towards a hawkish stance, as the inflation embers were heating up amid a resilient economy. But this week’s news on the inflation front has caused some rethinking of the issue, particularly among traders. Just one week ago, the widely followed CME tool assigned a 34 percent probability that the Fed would raise interest rates at its upcoming meeting on July 28-29. By this Friday, those odds shrank to 10 percent.

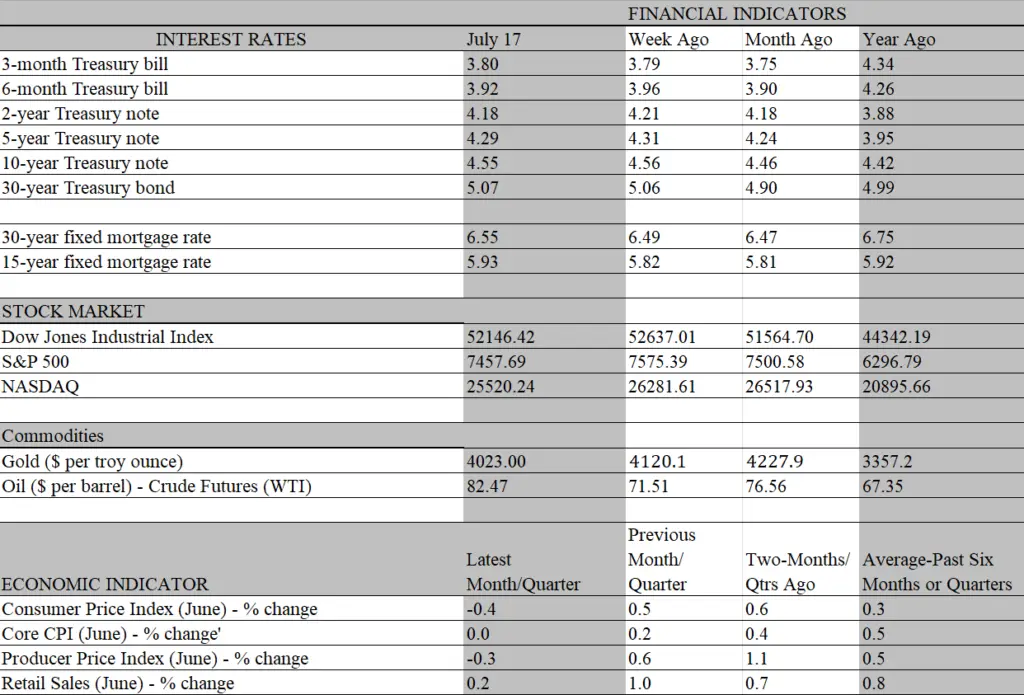

To be sure, no one is expecting a rate cut at the next meeting as the Fed is widely expected to keep the federal funds rate at its current 3.50-3.75 percent range. What’s more, there are no signs that the economy needs help from a looser policy although the struggling housing market would certainly benefit from lower mortgage rates. But this week’s benign report on consumer prices clearly took some steam out of the rate-hiking argument. Led by a steep decline in energy prices, the overall consumer price index fell by 0.4 percent, the first outright decline since the pandemic in 2020. Importantly, the sharp runup in oil prices heading into June has not bled into most other prices yet, as the core CPI was unchanged for the month. Indeed, unrounded – viewed beyond the first decimal – the core index slipped, marking the first time since April 2020 that both the overall and the unrounded core CPI fell together.

Looking beyond the next meeting, the jury is still out as to what the Fed’s first decision under the leadership of Kevin Warsh will be. Warsh has eschewed forward guidance as a means of communicating policy intentions, noting among other things that such guidance is usually influenced by stale data that could lead the Fed down the wrong path. The June CPI report is not only stale, it is rancid, as the main catalyst that dragged the overall index down last month is already driving it up, thanks to the resumption of attacks between the U.S. and Iran. The renewed flareup has sent crude oil prices up by 20 percent over the past week and prices at the pump are following suit. Both sides show no sign of letting up, pointing to sustained increases until cooler minds prevail and another ceasefire is struck. We wonder, however, if such a halt to hostilities would generate more skepticism than relief, given the tenuous nature of past agreements and the publicly expressed mistrust between the negotiators.

That said, there is more to the latest CPI report than the headline. True, one month does not make a trend, but some key details in the report suggest a more durable disinflation process is taking place. For one, housing costs, which comprise about one-third of the overall CPI and 40 percent of the core CPI, continue to retreat and is likely to be a formidable inflation anchor in coming months. Shelter prices rose by a slim 0.1 percent during the month with rents on primary residents increasing by the same amount. New lease signings indicate that rents are continuing to ease as multifamily housing is coming on stream at a rapid pace, highlighted by a 75 percent surge in starts last month. The increased supply of apartments should continue to take pressure off rents and offer a viable choice for first-time home buyers who are priced out of the market.

What’s more, the war-induced volatility in energy prices obscures the fact that 47 percent of prices in the consumer price index actually fell in June, the largest share in almost two years. Importantly, the Fed closely monitors prices of services, as they are more labor intensive, account for the largest share of consumption and are more reflective of underlying economic conditions. The core service index, which excludes energy and housing prices, increased by a tame 0.8 annual rate over the past three months. This confirms that labor costs are not a source of inflationary pressures and that pricing power of service providers is constrained, despite healthy demand by high-net-worth households.

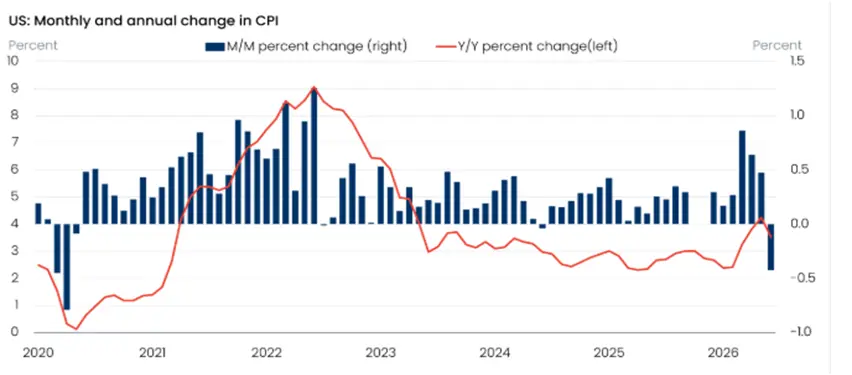

Simply put, the benign inflation reading last month reflects more than just the temporary plunge in gas prices. But that plunge has significance for the broader economy. Just as higher gas prices act as a tax on consumers, lower gas prices does the opposite as it frees up funds that can be used for other purchases. That boost to purchasing power was clearly evident in June’s retail sales report. Overall sales rose by a modest 0.2 percent in June, held down by the plunge in price-related gas station sales. But excluding gas, retail sales staged a robust 0.7 percent increase. And about 60 percent of those sales enter the personal consumption component in the GDP accounts. This so-called control group of sales rose by an even more impressive 0.8 percent in June. As a result, the second quarter’s GDP should receive a sturdy boost from consumer spending, which is tracking around a 2.5 percent growth rate.

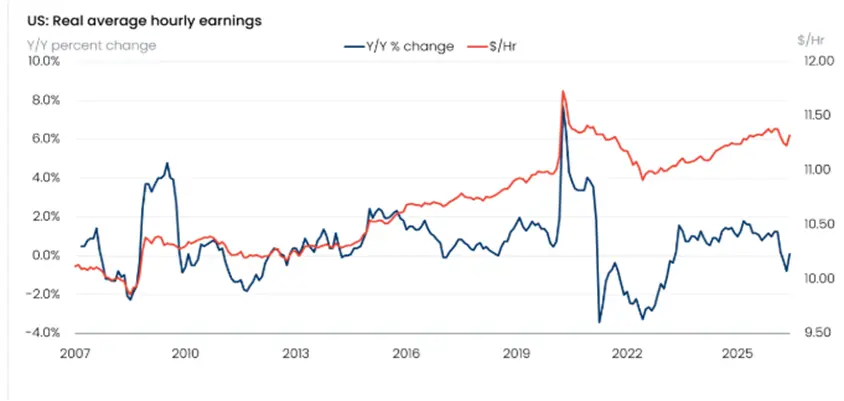

However, the negative tax impact from higher gas prices will reappear in July unless an unexpected end to the Mideast conflict suddenly appears. The drag on overall consumption depends on several things, most notably how financially equipped households are to handle the rebound. With savings depleted and tax refunds mostly spent, the major source of purchasing power for most households will come from earnings. Due to the war-induced surge in gas prices from March through May, inflation outpaced wage growth, leading to a drop in real earnings. That trend reversed last month with the plunge in gas prices lifting real earnings for the first time since January. Odds are that temporary relief will be undone in July, as the rebound in prices at the pump will again take a bigger bite out of incomes.

In short, the Fed’s first move under the new Chair remains unsettled. The case for breaking precedent with a rate cut received a boost from the benign June inflation report and signs that an enduring disinflation process is set to begin. But despite constraints on real incomes, consumers remain resilient, buoyed by wealthy households benefiting from strong asset gains and a surprisingly healthy job market that allows workers to sustain spending despite slowing wage growth and meager savings. The Fed’s dilemma is further amplified by the uncertain future of AI-driven investment spending. It is a powerful force driving the current and near-term growth outlook – as well as the stock market – but is vulnerable to myriad headwinds, such as earnings that do not justify overzealous spending, a public backlash and a bearish pivot by investors that could bring market values – and the wealth effect — crashing down. Given this fluid economic landscape, the probability the Fed will remain on a protracted hold until a clearer picture appears is the most reasonable bet.