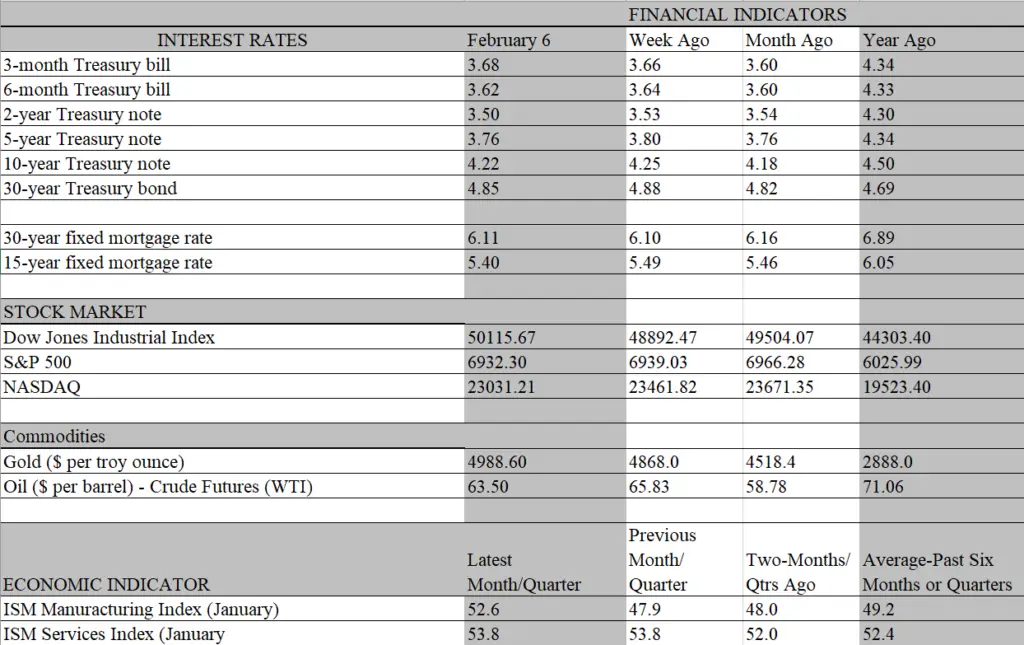

To say it was a topsy-turvy week in the markets would be an understatement, as extreme volatility buffeted stocks, bonds and commodities. Gold and silver suffered their biggest one-day plunge in over 35 years to start the week, after hitting record highs at the end of the previous week. Similar, if less extreme, daily swings were also seen in stock and bond prices. Such wild movements are usually linked to some unexpected or sudden shock; but no obvious source of heightened trader angst seemed to stoke the fires this time. Uncertainty over monetary policy, the job market, inflation, tariffs and geopolitical developments continued to simmer, but none showed signs of boiling over. The one catalyst gaining traction is concern over the AI boom, reflecting growing fears that the exuberant business spending on AI technology will not reap the expected rewards. Unsurprisingly, the stocks of public companies heavily engaged in such spending were severely punished for a while, but they staged an astonishing rebound on Friday, sending the broad market to new highs.

Given their extreme volatility, it would be foolhardy to predict the future performance of these stocks. Yet where they head matters because of the outsized contribution that the wealth generating rally in those stocks have made to economic growth over the past year. Most of that wealth has been garnered by older and richer households who have been the main drivers of consumer spending. To be sure, it is too early to tell if the recent slump in AI stocks was simply a time-honored correction in an overpriced sector or if Friday’s surge reflected dip buying by traders exploiting a perceived opportunity. But this week’s action is a vivid reminder that the stock market travels a two-way street, and the wealth gains that have powered growth could just as readily morph into an economic drag should the market sputter.

What’s more, that potential drag could become something more serious if the exuberant investment spending on AI technology does not generate the lucrative rewards expected from that spending. If the payback falls short of expectations, the capital spending spigot could narrow considerably if not close, removing another major source of support from the economy. It was reported this week that the five largest tech companies plan to spend about $700 billion on AI technology this year, which is poised to give GDP a major boost in coming months. If the expected returns do not materialize, those spending plans could well be trimmed, lowering the economy’s growth prospects later in the year and sapping strength from the trend in earnings that has powered the stock market gains.

And as is the case in the financial markets, it’s risky to bet on what’s causing recent developments in the real economy. For example, it is unclear whether the evolving slump in hiring is largely a correction of the over hiring of workers during the pandemic recovery, when labor shortages were a major business concern, or if something more fundamental is at play. No doubt, the drive to remove bloat is playing a role, but companies would not be curtailing job openings to such an extent if they had a brighter view of sales prospects. We will get a better sense of actual hiring next week, when the Labor Department releases the January employment report, delayed from this Friday because of the brief government shutdown.

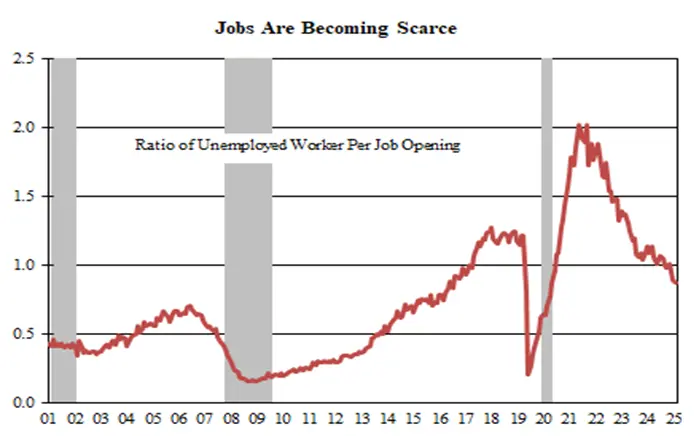

But the agency did release the JOLTS report that covers key indicators of labor market conditions through the end of December this week. The most eye-opening data point was the plunge in job vacancies posted by companies, considered a proxy of staffing needs and hiring intentions. The outsized 386 thousand drop in job openings in December far exceeded expectations and followed two consecutive months of reduced job postings. Hence, at the end of the year there were only 87 job openings for every 100 unemployed workers. That’s the lowest ratio since March 2021 and, needless to say, unemployed workers are having a difficult time finding a job.

The good news is that the hiring rate stopped its relentless drop in December, edging up from 3.2 percent to 3.3 percent. The bad news is that it has stabilized at a historically low level. With job openings in the doldrums and hiring sluggish, workers are staying put instead of voluntarily quitting and risk not finding a better position elsewhere. That combination of low attrition and reduced hiring means that if companies want to reduce headcount further, they will have to stary laying off more workers. So far, that has not happened on a broad scale, despite some high-profile layoff announcements recently. The JOLTS layoff rate remains historically low and jobless claims reported by state unemployment agencies are also subdued. But the portents are ominous. The large outplacement firm, Challenger, Gray & Christmas reported its regular tabulation of job cuts this week, which included the largest round of layoffs for the month of January since 2009, in the midst of the Great Recession.

Meanwhile, the large payroll processing firm, ADP, reported a big drop in private job growth in January, to 22 thousand from a 55 thousand average in November and December. We expect that the upcoming monthly employment report from the Labor Department will show a similar sluggish pace of job creation in January, although the figure will contain a lot of noise from bad weather, a nurse’s strike in NY and a flu outbreak that kept workers from their jobs. Importantly, we don’t expect to see a visible increase in the unemployment rate from the 4,4 percent posted in December. One reason: net migration out of the U.S, due to the immigration crackdown continues apace, removing foreign born workers from the labor force. Hence, the slowdown in job growth is being matched by the slowdown in the supply of workers, lowering the number of new jobs needed to prevent a rise in the unemployment rate.

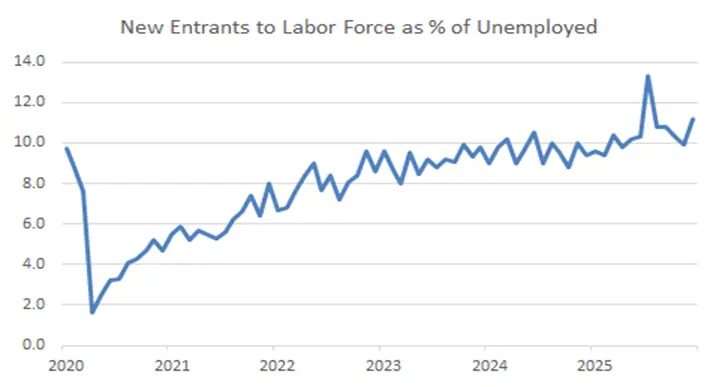

We estimate that only about 20 thousand new jobs a month are needed to keep the unemployment rate from rising. To be sure, the unemployment rate has risen by about a percentage point from its cyclical low of 3.5 percent. But a large portion of the grind higher in the unemployment rate can be traced to workers entering or reentering the labor force and finding it harder to secure a job. Younger workers, particularly Gen-Z and recent college graduates, have been particularly hard-hit. Only a small portion of the increase can be traced to permanent layoffs. If the flood of new job seekers overwhelms the demand for workers, you can expect the unemployment rate to embark on a sustained upward climb. We don’t expect that to happen anytime soon, if only because the economy will be getting a big fiscal jolt from tax refunds in coming months, which should keep the demand for workers at least at current levels. Later in the year, however, when the refunds are spent and job creation slows, the stage will be set for a weaker job market, and spur the Fed to resume its rate-cutting campaign.