Tensions are escalating on a number of fronts, from military developments, conflicting economic data and, somewhat surprisingly, a Supreme Court ruling on Friday upending the administration signature trade policies. The ruling, which disallowed the administration’s use of emergency powers to justify the avalanche of tariffs over the past year, was not entirely unexpected, but it does point to a policy reset. To be sure, the administration has other vehicles to impose tariffs and will use them aggressively to avoid refunding the tens of billions collected from businesses. Companies, large and small, have been lining up to file claims for refunds and are now speeding up those efforts. Unsurprisingly, Trump quickly announced his intention to impose a new 10 percent replacement tariff, using another lever at his disposal.

It remains to be seen if the Supreme Court’s decision distracts the president from his focus on the Iran imbroglio. As of Friday morning, Trump gave Iran 15 days to strike a deal or “bad things will happen.” Nothing is more disruptive to financial markets – and confidence on Main Street – than a war, and it is remarkable that the market response so far has been relatively tame. Uncertainty is a time-honored catalyst of volatility, but it often ushers in inertia until things are sorted out. Meanwhile, fresh economic data is not providing more clarity on the economy’s performance. That’s particularly upsetting to a Federal Reserve that is still uncertain which is the greater risk to the economy, faster inflation or slower growth dragging down the job market.

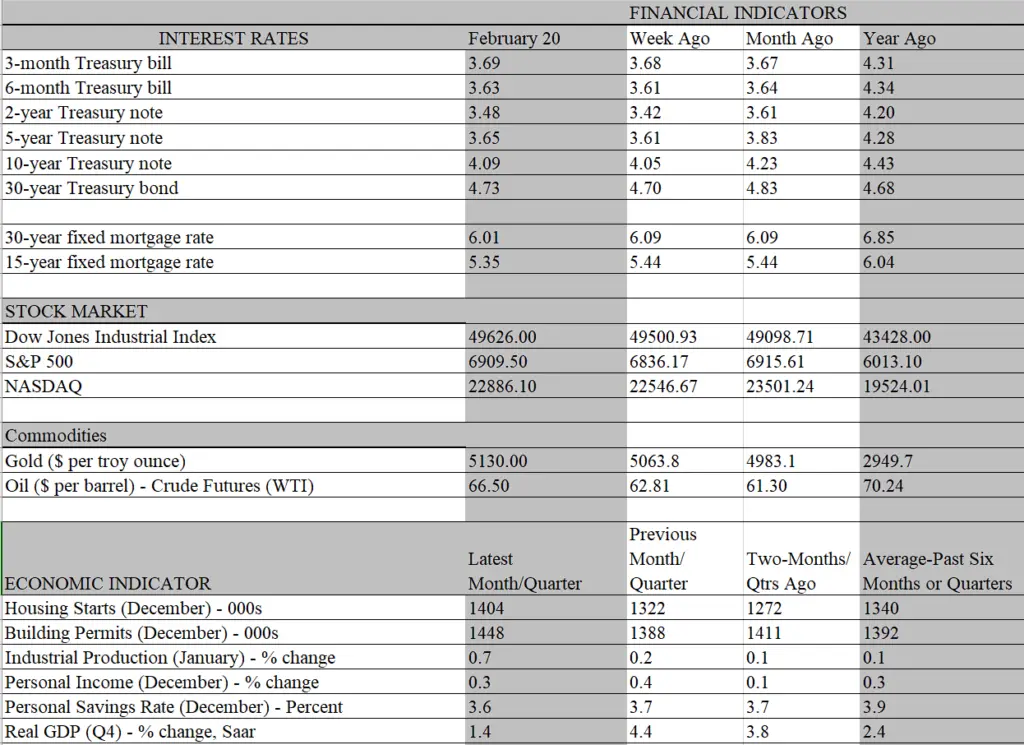

The data flow cast a spotlight on both sides of the ledger this week but did little to answer which of the risks is greater. Prior to the data releases, the minutes of the January Fed policy meeting were revealed; importantly, they portrayed a more hawkish sentiment among officials than expected, with some discussing the possible need for a rate hike this year if inflation remains sticky and the economy resilient. Traders had already pushed back on the prospect of a near-term rate cut, thanks in good part to the subsequent jobs report showing a blockbuster payroll increase in January. But few were prepared to hear that a rate hike was even on the table. The odds of rate increase this year remain highly unlikely in our view, but inflation concerns were validated in some of the data released this week.

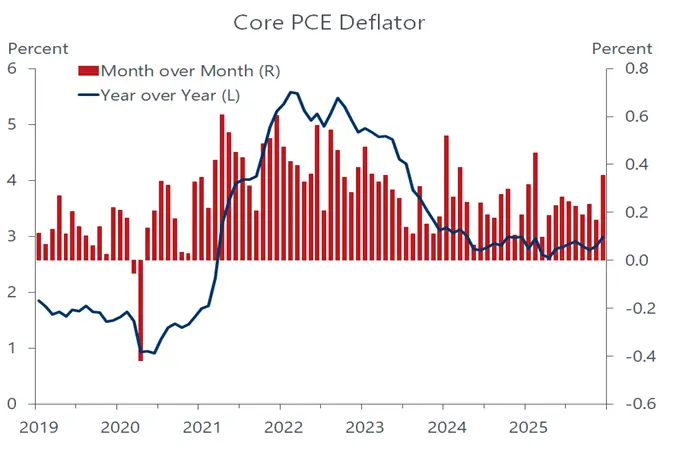

In particular, the Fed could not have been happy to see its preferred inflation gauge, the personal consumption deflator come in stronger than expected. Both the overall and core PCE increased 0.4 percent in December from the month before, the strongest for a month since February. Compared to a year ago, the headline PCE deflator rose 2.9 percent and the more important core deflator, which excludes food and energy items, increased 3.0 percent – the first time it touched 3 percent since April 2024. More important is that the deflators are moving further away from the Fed’s 2 percent target, raising a big obstacle in the way of a rate cut.

While some of the upward pressure came from tariffs, that is not an immediate concern for Fed policy. For one, the bulk of the tariff impact is behind us and the prospect of renewed pressure from this source has been diminished by the Supreme Court decision. Indeed, in the unlikely event that the roundly $150 billion of tariffs collected so far were to be refunded to companies, some might be passed on to consumers in the form of price cuts. Of more concern is the sticky inflation on services, which are less exposed to the tariff effect. The Fed pays particular attention to core service prices, which exclude housing costs. This so-called supercore index has recently turned zestier, increasing at an annual rate of 3.9 percent over the past three months.

From our lens, the hotter than desired inflation pace now seen in the data will cool as the year progresses. As noted, the tariff impact on goods prices is mostly over, even as the impact has been milder than expected. Service prices are heavily influenced by housing and labor costs; both are poised to cool in the months ahead. Housing costs have been slowing for some time and forward-looking data on market rents augurs for a continuation of that disinflationary trend. Likewise, the main influences on labor costs also point to less inflation pressure. Despite the aberrational surge in job growth recorded last month, labor conditions are weakening. There are more job seekers than job openings, hiring has stagnated, workers are staying put instead of quitting in hopes of getting a better-paying position, and unemployed workers are taking longer to find a job. Collectively, these are powerful constraints on worker bargaining power.

The angst of workers is exacerbated by the prospect they will be replaced by the surge in labor-savings investments in AI-related capital equipment, software and robots. The productivity gains already underway have contributed mightily to the economy’s growth over the past year, reinforcing the impetus provided by the outlays themselves, particularly those linked to the construction of data centers. An unanswered question is whether the disinflationary effect of stronger productivity will offset the inflationary impact these energy-hogging data centers are causing, including driving up electricity costs. That said, the continued strong productivity gains last year undoubtedly helped restrain inflation amid another year of solid growth and low unemployment.

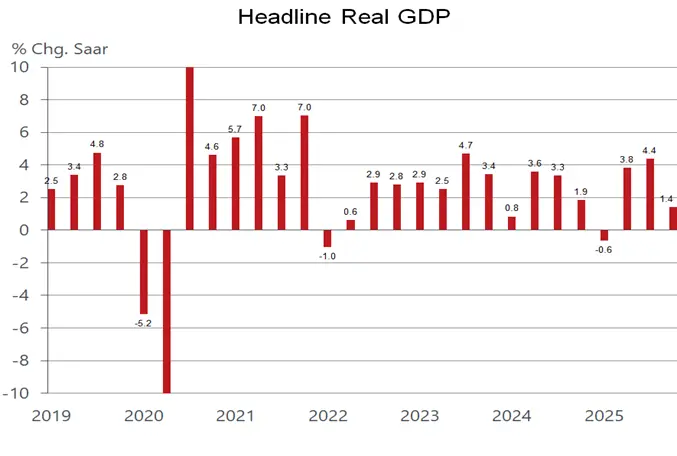

On the surface, it would appear the economy’s growth engine downshifted markedly in the fourth quarter, as GDP logged a tepid 1.4 percent growth rate during the period. That’s a big step down from the 2.4 percent average pace over the first three quarters of the year. But all of the decline, and then some, reflected a 1.1 percent drag from the record long government shutdown, slicing a huge chunk of working hours from Federal payrolls as well as the temporary removal of their paychecks. Underneath the hood, however, the main drivers of the growth engine were still operating on all cylinders. Consumers remained resilient, upping spending at a sturdy 2.4 percent pace and business nonresidential outlays increased by a formidable 3.7 percent.

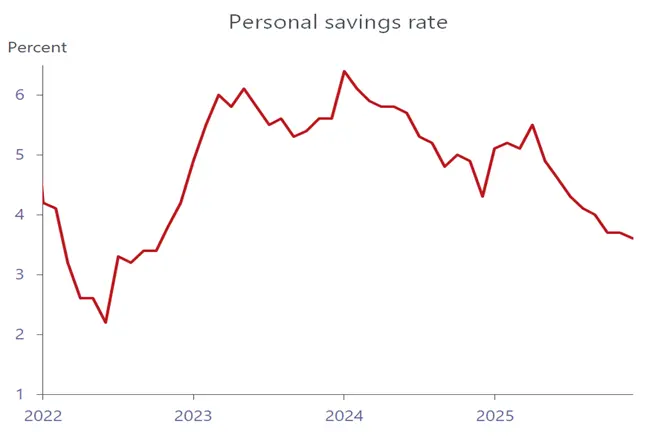

With the government back to full strength, except for the partial shutdown related to DHS spending, the lost working hours and paychecks are being reclaimed, setting the stage for a rebound in GDP in the first quarter. However, the one cautionary signal from the latest monthly income and spending report is that consumer spending continues to outpace income growth, which after taxes and inflation has turned negative over the last three months. Hence, households are increasingly drawing on savings to support purchases, driving the personal savings rate down to the lowest level since October 2022. This decline reflects in part upper-income households spending more of their paychecks, comforted by the wealth gains they enjoyed from surging stock portfolios. That wealth effect should continue to be the main driver of consumer spending this year, barring a wealth-destroying setback in the market. What’s more, lower income households will be getting some relief in coming months from above-normal tax refunds. Simply put, far from running out of gas suggested by the tepid GDP growth rate in the fourth quarter, consumers and businesses should provide enough spending and investing fuel to power the economy’s growth engine this year. And, with inflation expected to resume its cooling trend, some further help should be coming from Federal Reserve rate cuts later in the year.