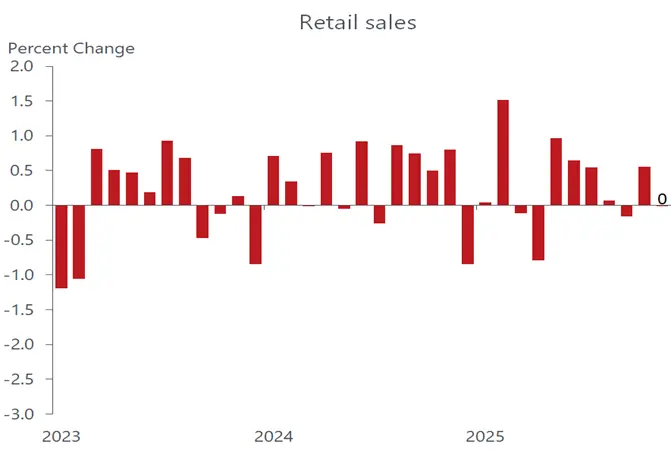

Like the fictional King of Siam who grappled with what he knows and what he doesn’t know, so too must economists as well as the Fed view this week’s batch of data as a”puzzlement”. The January employment report flpped the no hiring/no firing narrative on its head; the December retail sales report upended notions that wealthier households were still driving a torid pace of consumer spending; and the consumer price report for January refuted the hawkish view that the glue underpinning sticky inflation remains as tacky as ever. Such confusion often leads to inertia, and we suspect that there will be no knee-jerk policy reaction to any of the week’s reports.

Taken together, the broad theme suggested by the December/January data is that activity ended 2025 like a lamb but came roaring back like a lion in 2026, whilst inflation remained as calm as a deer. As we write this on Friday the 13th, our skepticism over the veracity of this theme is only enhanced. For one, the months around the turn of the year are always more suspect than others as outside noise has more of an impact on hiring, pricing and spending than does human behavior. It’s always the case that one month does not make a trend, and both December and January are particularly vulnerable to weather disruptions, faulty seasonal adjustments and tentative reassessments of existing plans for the new year amid heightened uncertainty.

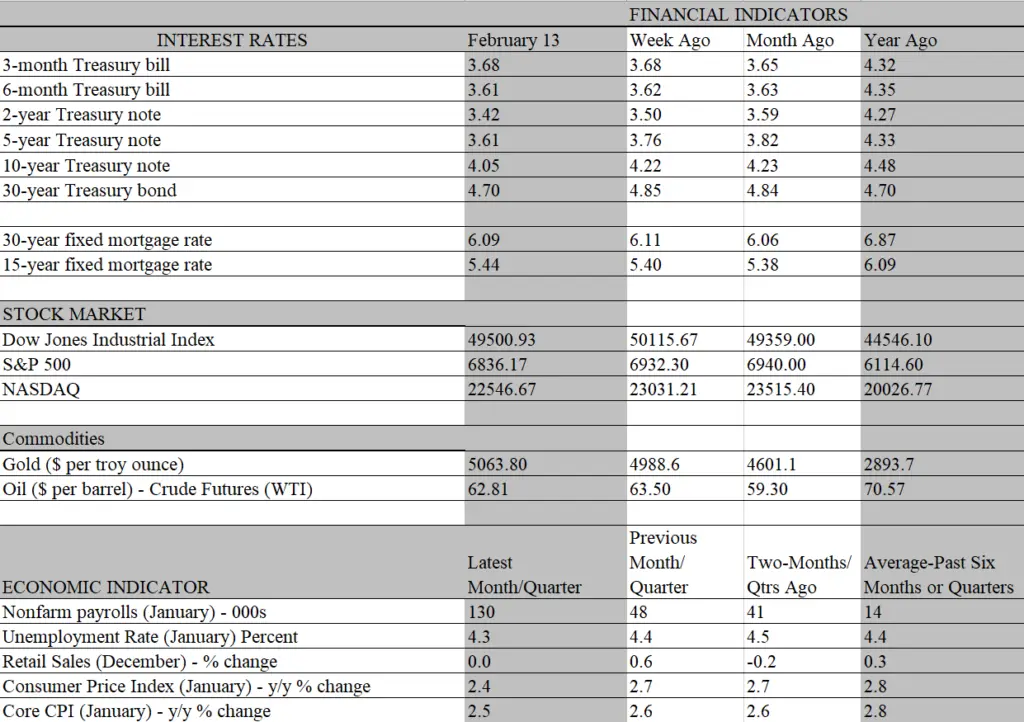

Importantly, each of the key reports this week conveys messages that are not supported by unfolding developments and are unlikely to be sustained. There is no reason to suspect that consumers have closed their wallets and purses for good, as indicated by flat retail sales in December. True, that was far weaker than consensus expectations and it followed downwardly revised sales figures for the two previous months. But the loss of momentum at the end of the year comes on the heels of robust spending in the second and third quarters, which far exceeded expectations. It’s understandable that consumers took a breather in the closing months, as many goods were purchased earllier in the year to avoid tariffs and they incurred higher debt loads that households decided to manage instead of shopping for more goods. Indeed, credit card debt surged by nearly $14 billion in December, the largest monthly increase in more than two years.

That debt bulge is enough of a sticker shock to encourage a spending pause for low-and middle-income consumers, whose deeply pessimistic view of economic prospects are already at odds with profligate shopping behavior. Keep in mind that retailers mainly sell goods while service providers account for the bulk of consumptions in the U.S. These providers, in turn, cater mostly to wealthier and older households, who have been the major drivers of consumer spending, fueled by the enourmous gains obtained from their stock holdings and rising home values. We expect that the weakness in retail sales was flattered somewhat by spending on services revealed in the upcoming personal income and spending report for December.

That said, miserable weather conditions may have short-circuited a spending rebound in January, as potential shoppers spent much time digging their cars out of mountains of snow and staying in heated homes instead of venturing out in one of the most frigid months in recent memory. But the seeds of a resumption in spending have been sown, and we expect greenshoots to sprout in coming months. For one, household bank accounts will shortly be fattened with a formidable stream of tax refunds and credits stemming from last year’s One Big Beautiful Tax Act. No doubt, lower and middle -income households will use a chunk of those funds to pay down debt, but some of it may also be used to retake purchases they were forced to miss in December. While wealthier households will be receiving the largest share of the tax refunds, they have a lower propensity to spend out of each additional dollar of income. Hence, the economy will receive a smaller bang for the buck from those tax breaks.

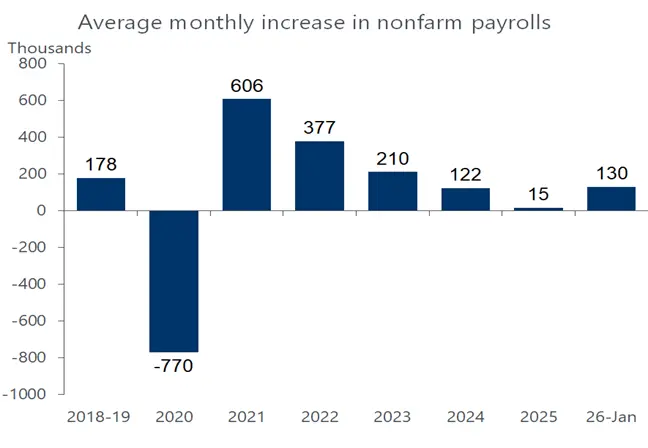

Importantly, lower-and middle-income households depend heavily on income from wages and salaries to support spending. If the blockbuster jobs report for January is any indication, they received a big jolt of purchasing power to go on a shopping binge. The headline-grabbing 130 thousand surge in nonfarm payrolls took just about everyone by surprise, as job growth practically ground to a halt in 2025 and most expected the January increase would be less than half the reported gain. The payroll spurt belies the first half of the “no hiring/no firing” narrative that has come to decribe the job market. What’s more, a dip in the unemployment rate from 4.4 percent to 4.3 percent added to perceptions that the job market is running hotter than generally perceived.

But we caution not to read too much into the muscular headlines attached to the report. A strong job market would be characterized by sustained increases spread across a broad range of industries. That’s hardly the case now, as only a few industries are powering the job gains. Leading the list is the health and social services sector, which as has been the case for over a year, has generated more jobs than the economy as a whole. In January, it’s share slipped a bit, but still contributed an outsized 124 thousand, or 95 percent of the 130 thousand increase in payrolls. More broadly, job gains of this magnitude are not sustainable as there are just not enough workers to fill positions. We estimate that the increase in the working age population has been drastically cut to about 20 thousand a month, reflecting reduced immigration and an aging population that is spurring a wave or retirements.

We note that the very sector that is powering the biggest job gains is highly vulnerable to the government’s immigration crackdown. According to the Migration Policy Institute, immigrants acccount for almost 40 percent of home health care aides and nearly 30 percent of personal care aides. It’s not clear how many of those workers are unauthorized; but should they be identified and deported, the squeeze on the healthcare sector would tighten, pushing up labor costs and the already high cost of health care for millions of Americans. Outside of this sector, however, the demand for workers is running far under the pace of job gains seen in the January report, which leads us to believe that the 130 thousand increase is far above what is sustainable. The number of job openings has fallen below the number of job seekers, companies are striving to normalize staff after the overhiring during the pandemic and the surge in AI spending promises to boost productivity, replacing labor to generate output.

Unlike the retail and jobs data, the key inflation report for January is one that did not offer much in the way of surprise. Consumer prices cooled a bit more than expected, raising hope that the disinflation process can resume and gradually trend towards the Fed’s 2 percent inflation target over the next year. That, in turn, should enable the Fed to cut rates two more times over the second half of the year, even as it stays on the sidelines now to assess the conflicting reports tracking the economy around the turn of the year. The good news is that usual weakening in economic activity that accompanies cooling inflation – and presages recessions – is not likely to occur this time. With the job market in better balance, wages should hold up as inflation retreats, pointing to improving real incomes for workers. Indeed, with fewer workers joining the labor force in coming years, existing workers may well be asked to put in longer hours. The implications for worker purchasing power were already evident in January when the combination of a longer work week and a decent 1.5 percent year-over-year increase in real hourly earnings generated the strongest monthly increase in real wages since March 2021.