The weekly commentary will not be published over the Labor Day weekend. The next issue will be published on September 5.

All eyes were on the annual Jackson Hole symposium this week, hoping to see if Fed Chair Jerome Powell would provide any clue as to when, or whether, a rate cut would be coming. Unsurprisingly, the speech left the door open to myriad possibilities, but the markets clearly heard a dovish tone. Heading into the confab, expectations of a rate cut in September waned as the minutes of the July policy-setting committee released on Wednesday revealed more sentiment for a delay because inflation concerns still ran high among more committee members than thought. The following day, at least three Fed officials publicly suggested that a “wait-and-see” policy was appropriate.

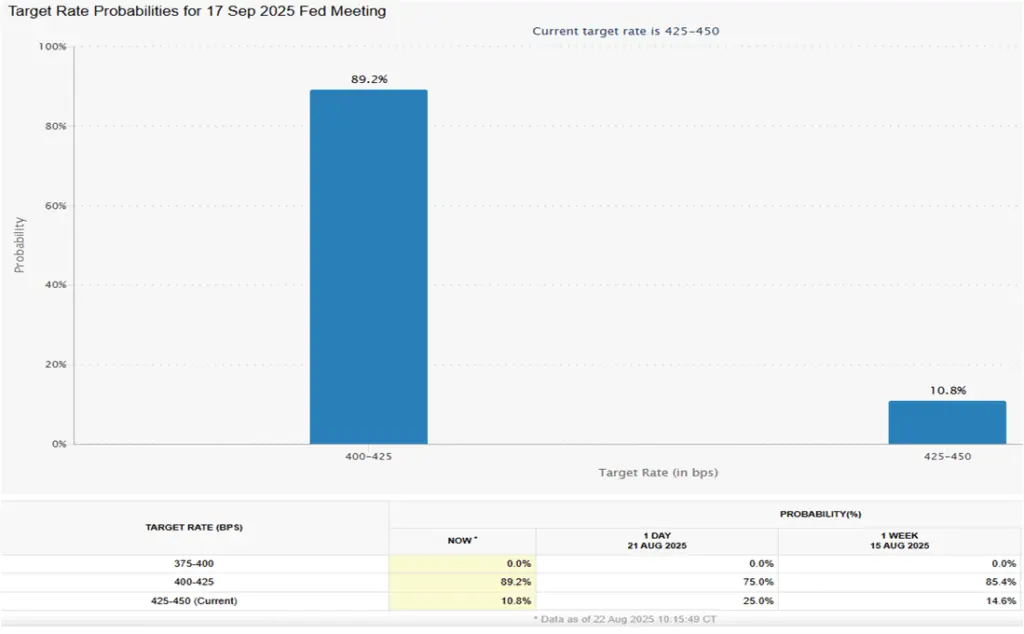

However, as Powell opened his remarks on Friday morning, the markets steadily priced in greater odds that a rate cut would take place at the next meeting in September. The shift in expectations shortly after Powell started speaking can be seen in the widely followed CME’s rate setting tool reproduced below. Fifteen minutes into his talk (10.15 am), the probability of a quarter-point rate cut in September (from the current 4.25-4.50 % range to 4.00 to 4.25%) jumped to nearly 90 percent from 75 percent the day before. That brought the odds back to above where it was a week earlier, before the hawkish comments by the officials noted above were made public.

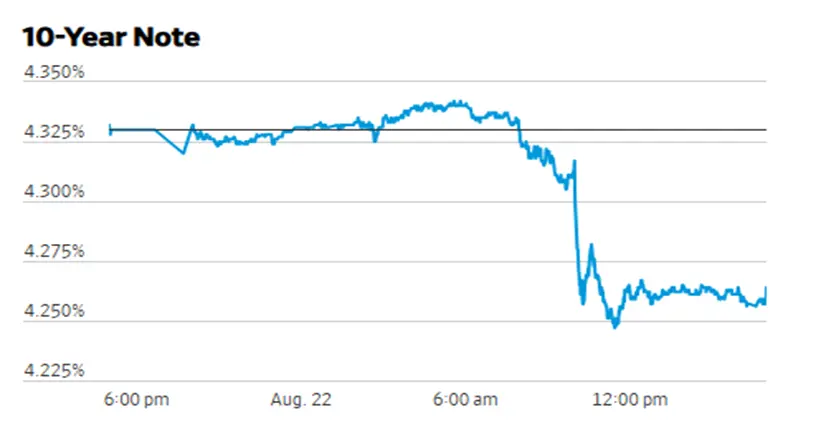

To be sure, Powell never said, nor would he, that a rate cut next month would take place. But analysts are prone to dissecting the language of Powell’s remarks, looking for any nuance that might suggest a departure from current expectations. This time was no exception and there was enough substance to parse out of the speech that moved the markets. Stocks rallied sharply on Friday and market yields turned lower. The key phrase that drew the most attention of traders was: “the shifting balance of risks may warrant adjusting our policy stance,”. Simply put, the Fed chair is paying more attention to the risk that the job market may deteriorate faster than thought, something that would be hard to arrest once it gains traction.

Powell recognizes that the unemployment rate remains at a historically low 4.2 percent. But he also said that the job market is in a “curious balance”, with both the demand for and supply of workers falling. Hence, the unemployment rate has not budged from its low level, despite the sharp downshifting in job growth to a monthly average of 35 thousand over the past three months from 232 thousand in January. Helping keeping the unemployment rate down is the fact that reams of people are leaving the labor force. That, in turn, is spearheaded by an astonishing outflow of foreign workers due to tightened immigration policies. Meanwhile, tariff uncertainty has put staffing decisions on hold, resulting in a reduced demand for labor.

As we have noted in the past, the low hiring, low firing mindset of businesses is not sustainable even if the unemployment rate remains near historical lows. Keep in mind that when more people are receiving paychecks, more people have the wherewithal to spend. Just the opposite is also the case. Fewer jobs mean less purchasing power to enter the spending stream. Less spending in turn, means less reason for employers to hire workers and more incentive to reduce payroll. Eventually, a cycle sets in that drives up the unemployment rate and ushers in a recession. This vicious cycle was tacitly spelled on by Powell when he fleshed out the “curious balance” statement, saying “Overall, while the labor market appears to be in balance, it is a curious kind of balance that results from a marked slowing in both the supply of and demand for workers. This unusual situation suggests that downside risks to employment are rising. And if those risks materialize, they can do so quickly in the form of sharply higher layoffs and rising unemployment.”

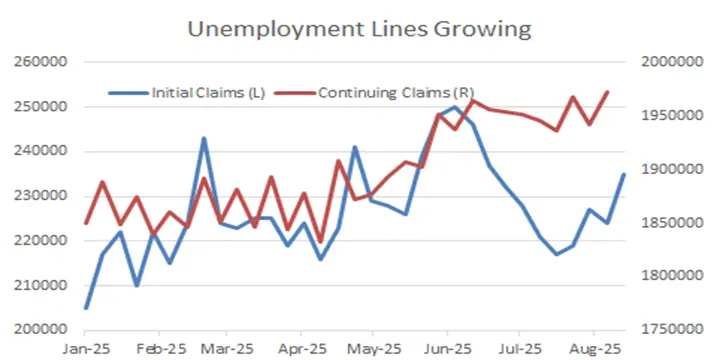

At this juncture, that risk is still remote as the conditions for widespread downsizing by companies are not in place. Households are being more selective in their purchases but are still spending. Jobs may be growing at a drastically reduced pace, but they are still growing. Importantly, higher income households who account for more than 50 percent of total spending – which drives about 70 percent of total economic activity – are enjoying sturdy wealth gains, punctuated by Friday’s massive rise in stock prices. That said, companies are feeling the pinch of higher tariffs, which are driving up costs of supplies that may eventually lead them to seek offsetting savings on labor costs. This may already be starting. Although one week of data may be more noise than substance, initial unemployment claims jumped 11 thousand in the latest week and the number of workers collecting benefits on a continuous basis continued to climb, reaching the highest level since November 2021.

Hence, Powell is taking a softer stance than the more hawkish tone sounded by other Fed officials in recent days. But that doesn’t mean he is ignoring the inflation threat posed by tariffs and the fact that prices are stubbornly rising faster than the long-held 2 percent inflation target. While he still believes that tariffs are likely to cause a one-time boost to the price level, not a sustained increase in the inflation rate, he acknowledges the risks to that perception. As he noted this morning, tariffs do not hit all at once, but on a recurring basis as they work their way through the supply chain. There is also the risk that workers may demand bigger wage increases as the boost to prices cuts into their real incomes. This, in turn, could result in the dreaded wage-price cycle that feeds inflation. However, given the nascent fissures opening in the job market, he also believes the threat of a wage-price spiral is weak.

From our lens, Powell is leaning towards an insurance rate cut in September to guard against a more severe deterioration in the job market than generally expected. But while a September move is likely, it is not a slam dunk. There are still another jobs and inflation report due to be released before the September meeting, and an outsized reading on any of the two could sway the decision of Fed officials who may be on the fence. One prospect Powell fears the most is an un-anchoring of inflation expectations, which would result in a self-fulfilling prophecy. So far, both survey and market expectations of inflation have been held in check, but that could change quickly if the Fed loses its inflation-fighting credibility. More than anything, that lessens the likelihood that any rate cut in September would be greater than a quarter-percent, something that President Trump is urging him to implement. In the current environment, such a move would likely backfire and cause a negative reaction in the financial markets.