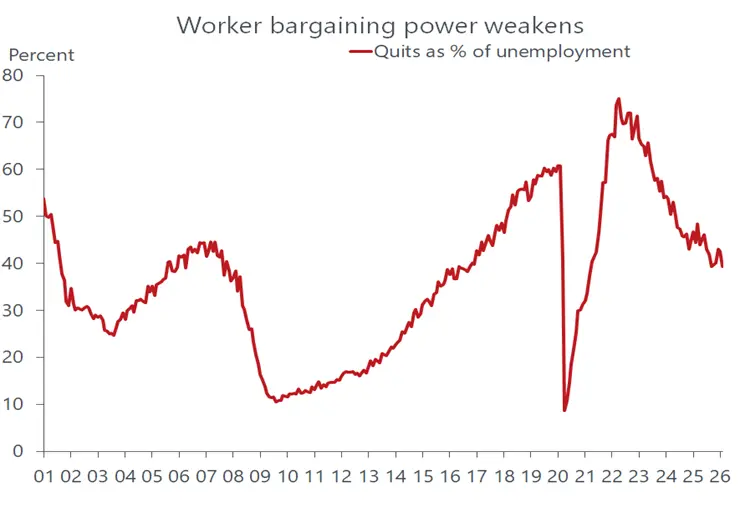

President Trump’s speech on nationwide TV Wednesday did little to calm the markets or provide assurance that the Mideast war will end sooner rather than later. The overriding impression garnered from his comments is that the prospect of an escalation of hostilities is just as likely as a diplomatic ceasefire. That left the markets mired in uncertainty and parsing through an array of starkly different scenarios based on the war’s progress. The market reaction on Thursday was just as peripatetic, slumping in early trading and almost fully recovering by the end of the day as traders were hesitant to make any bold moves ahead of a three-day weekend amid a very fluid geopolitical landscape.

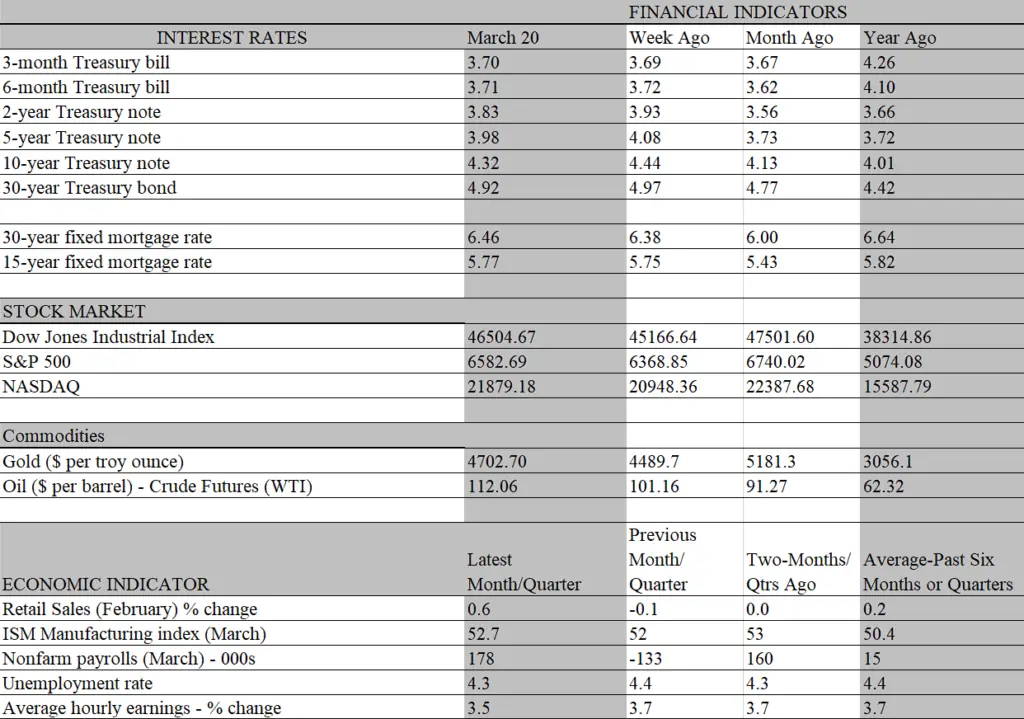

The turmoil surrounding the Mideast conflict overshadowed a raft of economic reports this week that would otherwise dominate the headlines. Most notably, the monthly jobs report suggested that the economy was in good shape as the hostilities began, as March payrolls jumped by an outsized 178 thousand, more than double expectations, and the unemployment rate fell. Revisions to the prior two months were almost a wash, with February turning out to be 41 thousand weaker and January 34 thousand stronger than previously estimated. Over the past three months, job growth averaged 68 thousand, which jumped from 3 thousand in February and is well above most estimates of the increase needed to prevent a rise in the unemployment rate.

We caution, however, not to read too much into the data as the disruptions caused by the war will have a material effect on both the growth and inflation sides of the ledger. What’s more, the March data on the jobs front give a somewhat misleading impression of labor market conditions. The return of 30 thousand workers from a nurses’ strike inflated the payroll gain in the health and social services sector, which once again rose by an outsized 90 thousand jobs, more than reversing a 28 thousand drop in February. This sector, which accounts for 15 percent of total employment, has been the main driver of job growth for several years. It continued to punch well above its weight in March, accounting for 50 percent of the increase in payrolls.

Likewise, the return of more normal weather after the harsh winter storms contributed to the sizeable increase in leisure and hospitality jobs from a slump in February. Importantly, there is good reason to be skeptical that April will see another month of job gains. Even without the disruptive influence of a war, there has not been two consecutive months of payroll increases since last May. That, of course, was a month after the Liberation Day tariffs were announced, ushering in a year-long period of economic volatility that is now being prolonged by the Mideast conflict.

Much like the jump in payrolls, it would be a mistake to read too much into the drop in the unemployment rate in March, from an already low 4.4 percent to 4.3 percent. That drop was not for the “right” reason, with job seekers on the unemployment lines suddenly finding work. The employed headcount, taken from a separate household survey, fell for the third consecutive month. More important is that the labor force continued to shrink; indeed, except for the pandemic blip, the labor force in March fell from the year-earlier level for the first time since 2013, reflecting the immigration crackdown and an ageing population. Neither of those influences is expected to improve in coming years, so the economy’s dependence on AI-driven productivity gains for growth – still more of a promise than a reality – will only deepen.

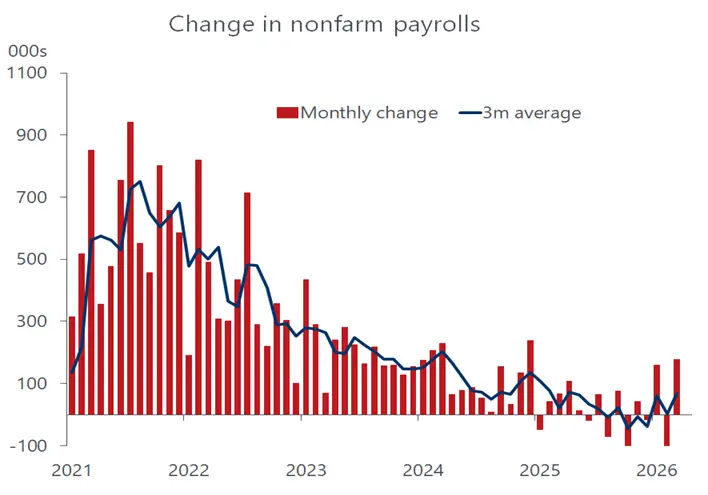

Simply put, under the hood of the headline blockbuster payroll increase and the aberrational drop in the unemployment rate, the labor market looks more fragile than sturdy. Worker earnings increased by a slim 0.2 percent in March and the advance over the past year slipped from 3.7 percent to 3.5 percent. That’s still a solid gain, but the slimmest since May 2021, when the economy was just emerging from the recession. Worse, even as wage increases are slipping, inflation is moving in the other direction and taking a bigger bite out of paychecks. This is hardly a prescription for stronger consumer spending. That’s particularly so for lower-income households who are more exposed to the war-induced price increases on gasoline and essential goods and services. Of note is that the increase in average hourly earnings for nonmanagement workers in March was less than for all private sector workers, clocking in at 3.4 percent over the past year.

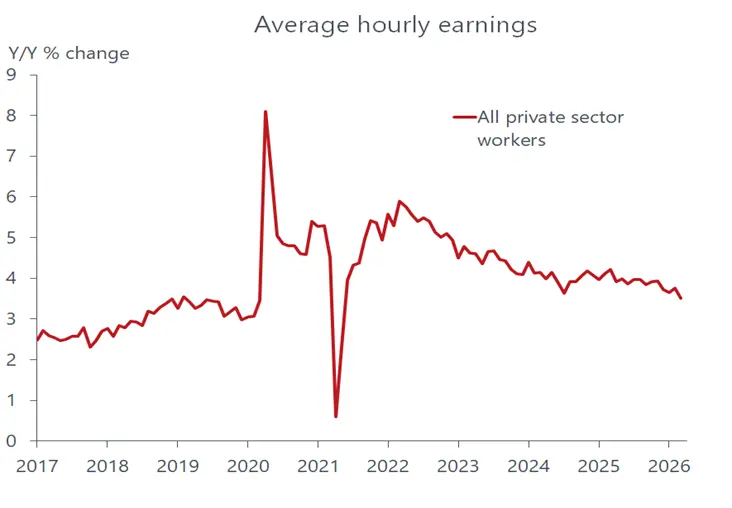

The good news for the macro economy is that the recent trend in earnings confirms that wages will not be a source of higher inflation. Nor should worker bargaining power strengthen anytime soon. The most visible evidence of that is the reluctance of workers to quit their jobs, believing that a better paying one could readily be found. The overall voluntary quit rate matches the lowest of the expansion. And except for the Covid plunge, the ratio of quits to unemployed workers is the lowest in more than 10 years. As much as anything, that highlights the profound shift in bargaining power from workers to employers that has taken place since the spring of 2025, when workers briefly flexed their bargaining muscle.

The bad news is that weakened bargaining power of workers translates into weaker purchasing power; since workers are consumers, their plight does not bode well for consumption, the economy’s main growth engine. So far, household wallets have not closed, as evidenced by the latest read on retail sales, which staged a solid 0.6 percent increase. That reading, however, was for February, well before prices at the pump leaped to over $4 a gallon and how the public’s negative reaction to the conflict will manifest itself at the cash register. We expect that the demand destruction from the war will take precedence over its inflationary impact in the eyes of the Federal Reserve and prod it to resume its rate-cutting campaign over the second half of the year. Even if the conflict lasts longer than is currently envisioned and stokes more inflation than the Fed feels comfortable with, the demand destruction would also intensify and heighten the recession odds. It’s important to remember that the Fed’s tools are equipped mainly to influence demand and has little control over a supply-induced shock to inflation stemming from an oil crisis.