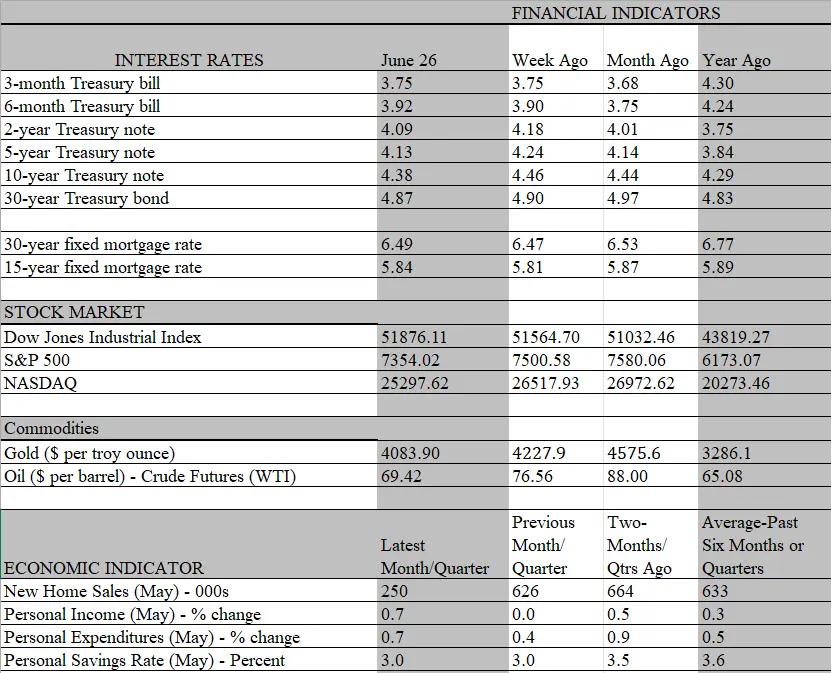

The plunge in crude oil prices since the ceasefire was announced on June 14 has been swift, much faster and deeper than most oil experts expected. As of Friday morning, crude quotes (West Texas Intermediate, or WTI)) fell below $70/barrel for the first time since early March and is barely $2/barrel above the prewar level on February 27. Prices at the pump are also falling but much more slowly reflecting the typical lag with changes in crude. It remains to be seen if the ceasefire will endure and allow organic forces in the oil market to fully play out. But the downward trend is timely, as it takes some of the sting out of recent inflation reports, which show just the opposite trend. To be sure, those reports, including this week’s release of the personal consumption deflator, the Fed’s preferred gauge, only captures readings through May, whereas the oil-price tumble did not start until mid-June.

That said, even if the price decline in crude is front loaded and remains around current levels, the catch-up phase on the retail level will continue. There is still a considerable way to go before gasoline prices, currently just under $4/gallon, return to the prewar levels of under $3/gallon. With the summer driving season just underway the demand for fuel is rising. What’s more, it will take time before service stations run down the more expensive fuel delivered earlier and refill their pumps with the cheaper gas. Still, a big chunk of the price decline so far will be captured in the June inflation readings, reversing some of the boost it imparted in May. About one-third of the .45 percent increase in the PCE deflator last month came from higher energy prices.

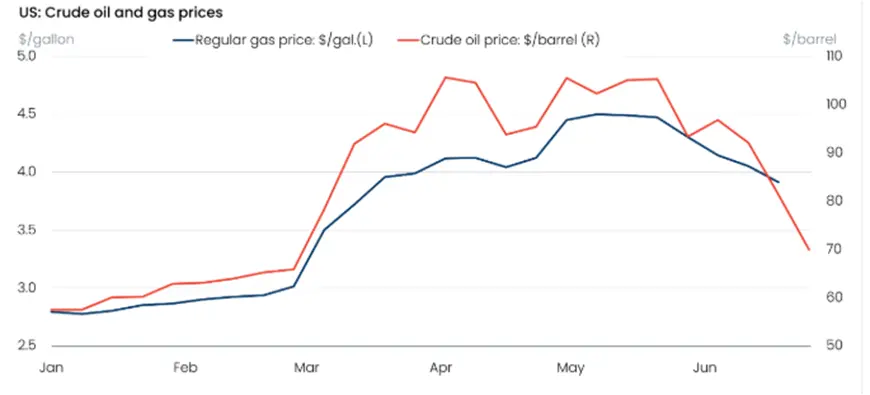

That month-over-month increase in the overall deflator lifted the annual inflation rate to 4.1 percent, the fastest since April 2023. Stripped of energy and food (which rose by 4.0 percent, and 0.3 percent, respectively), the core PCE increased by 0.3 percent over the month and 3.4 percent over the past year, the fastest annual increase since October 2023. Both came in as expected, so the market effect was relatively muted. Still, some of the underlying details were a bit worrisome, as the advance in service prices accelerated, something that keeps the glue in sticky inflation. The 0.5 percent increase in service prices equaled the fastest for a month since January 2024. However, in each of those monthly spikes, service prices were given a big boost by higher portfolio management fees, which is a volatile component. The hefty 1.2 percent increase in May followed a 0.3 percent decline in April.

We don’t believe the acceleration in service prices last month has legs, as it is not getting support from a key source: labor costs. Wage growth is slowing, and stronger productivity is restraining unit labor costs. Also, housing costs are becoming a big disinflationary influence thanks to the ongoing pullback of rent increases. Indeed, government statistics overstate rent increases because they include older as well as current leases. According to industry sources, such as Zillow and Realtor.com, year-over-year changes on new leases range between 1 and 2 percent.

A more sustainable source of inflation may be coming from the goods side, where the rapid build-out of AI technology is boosting costs of construction, computer chips, consumer electronics (note Apple’s recent announcement of huge price hikes on iPads and tablets), and electricity. The main restraint on the inflation-boosting-impact of AI seems to be coming from voters who are increasingly denying the approval of data centers in their districts. The big question is when and whether the expected productivity gains from AI will generate more of a disinflationary force than the inflation it is currently spawning.

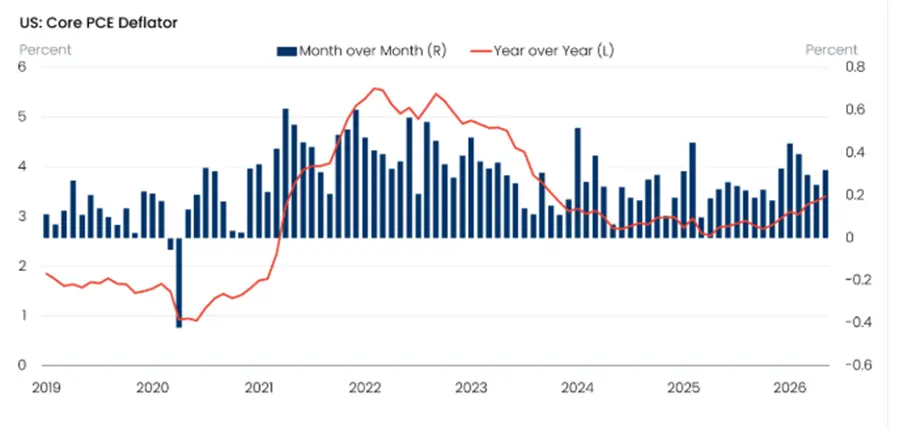

Importantly, the ongoing hot inflation data is not deterring consumers, whose continued resilience was on full display last month. Personal consumption increased by a sturdy 0.7 percent in May and by 6.3 percent over the past year; the annual gain is the strongest since January 2024. Some of the shine from those lofty increases, however, is dulled by sharp downward revisions to previous months. With inflation taking a 0.4 percent bite out of the nominal gain, real spending increased by a more modest, but still decent, 0.3 percent. Nonetheless the downward revisions pulled the average monthly increase in real spending over the first five months of the year down to a 2.0 percent annual rate, a marked slowing from the 2.6 percent monthly pace in 2025.

The slower pace of spending this year could be viewed ominously as it received a considerable boost from copious tax refunds that have just about run out. What’s more, real disposable incomes have shown no growth over the past year, and the personal savings rate is the second lowest in nearly twenty years. But we don’t see households zipping up their wallets in response to these developments. For one, the labor market is chugging along, delivering far more jobs this year than expected. For another, those pay checks will start to go a longer way, as we believe the peak in inflation was hit in May, and relief on the price front will steadily ease the squeeze on household budgets. The drop in gas prices will be a big catalyst, as it is tantamount to an immediate tax cut that will fill some of the void left from the removal of tax refunds.

Nothing in the recent batch of data will move the needle for the Federal Reserve over the near term. Inflation is still too elevated to justify a rate cut and emerging cracks in household spending power make consumers highly vulnerable to a rate increase. From our lens, the market is well ahead of itself in pricing in a 100 percent chance the Fed will raise rates this year. If, as we expect, inflation is poised to retreat starting this month and the Fed stands pat, real interest rates would increase and constrain economic activity. As we move closer to the end of the year, the pursuit of maximum employment should regain at least an equal footing with inflation in the eyes of the Fed, opening the door for a rate cut.