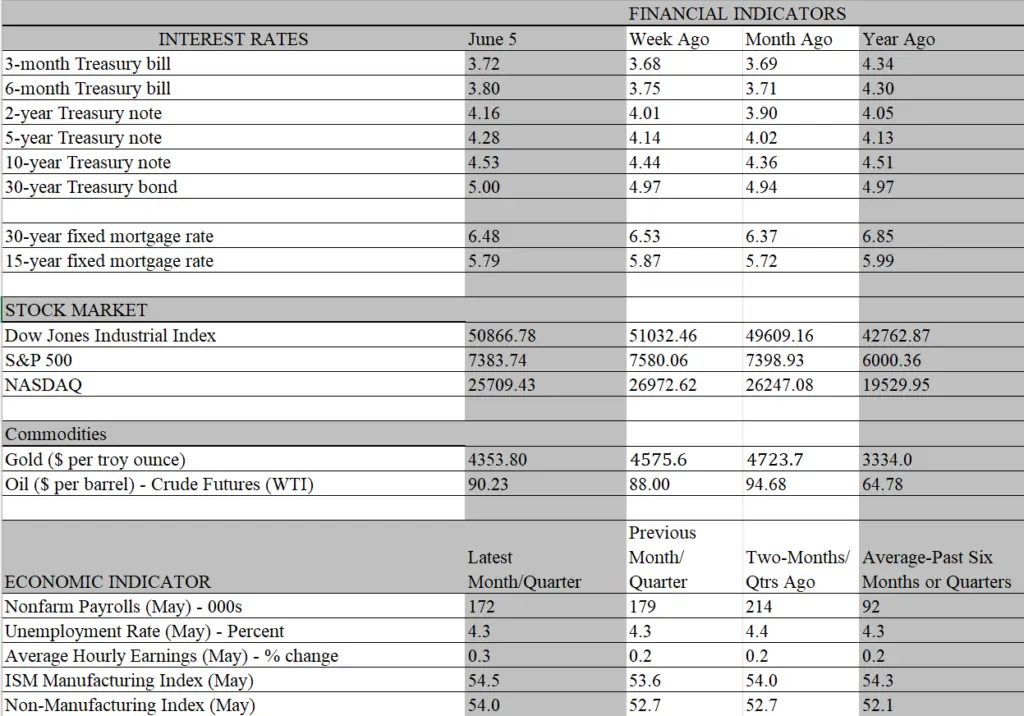

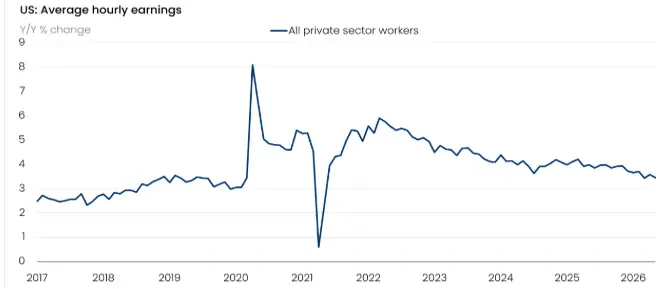

The official start of summer is still a bit more than two weeks away, but if the season mirrors recent economic data, it will be hotter than usual. All significant economic reports this week came in stronger than expected, punctuated by another blockbuster jobs report on Friday. Nonfarm businesses added 172 thousand workers to payrolls in May, more than double expectations and building on upwardly revised gains in March and April. Over the past three months, job growth averaged 188 thousand, a pace not seen in more than two years. For context, payroll increases averaged 42 thousand a month over the past year.

The eye-opening increase in job growth follows two surveys of purchasing managers this week that also depicted stronger than expected activity in both the manufacturing and services sectors last month. On the surface, therefore, it appears that that the Teflon U.S. economy is sloughing off the headwinds from the U.S./Israel war with Iran and is thriving despite the doom and gloom sentiment among households. Economists always warn that a single month does not make a trend. But a three-month stretch of stronger-than-expected data belies the notion that the job market is poised to fall off a cliff, which the dismal expectations of job and income prospects revealed in recent University of Michigan household surveys suggest.

The robust jobs data also call into question the headline-grabbing reports that AI is displacing workers in droves. Sifting through the data, only a glimpse of that impact appears to be unfolding, confined mostly to the finance sector, which was one of the few to see job losses last month. Overall, 54.4 percent of industries expanded headcount last month, the fourth consecutive month that more sectors were adding than subtracting payrolls. The broadening out of job gains is finally pulling in the manufacturing sector, where the percentage of expanding payrolls jumped to 53.4 percent. That is the first time more than half of factories increased headcount since February 2024, and the gain was the broadest going back to August 2023.

Indeed, there are signs that AI may be adding more jobs than it is displacing if hardhat workers are included with tech workers in the overall headcount. Construction payrolls increased for the third consecutive month, growing by 17 thousand in May. Unsurprisingly, given the moribund condition of the housing market, all of the increase and then some has been in nonresidential construction, which includes the booming demand for data centers. We note, however, that it takes many workers to build a data center, but only a few to run it when it’s fully operational. Hence, the longer-term prospects for these workers are questionable. Meanwhile, the displacement impact may be showing up elsewhere, shutting out wide swaths of job seekers from entering or reentering the workforce, particularly for entry level positions that are being automated.

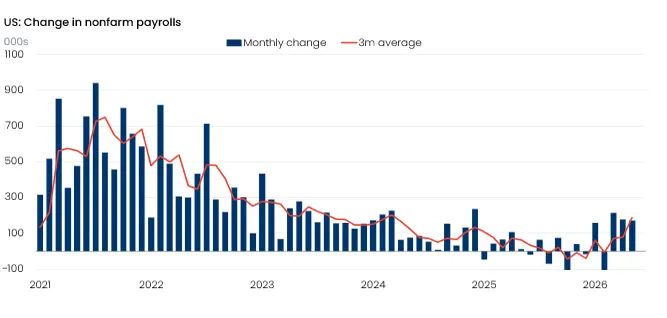

That impact is being overshadowed by the low unemployment rate, which remained at 4.3 percent in May. That rate is consistent with a fully employed economy, one that suggests anyone looking for a job can find one. But it conflicts with the boots on the ground around unemployment offices, where the long wait for jobless applicants to land a paycheck is reaching historic proportions. Last month, nearly 2 million workers were out of jobs for six months or longer, accounting for 25.7 percent of unemployed workers. That’s the highest share since the pandemic. Before that aberrational episode, you would have to go back ten years to find a larger share of job seekers unemployed for that long a period. What’s more, the ranks of the long-term unemployed may swell further as the share of workers out of a job for more than 15 weeks is rising just as dramatically, reaching 42.4 percent last month.

It is hard to reconcile the contradiction between the torrid payroll gains and the growing difficulty of unemployed workers to find a job. The most benign explanation is that it reflects a growing share of frictional unemployment, a time-honored occurrence when new technology is rapidly adopted by businesses and automates the functions of workers. Historically, those workers are retrained, relocated or find positions with other emerging industries, and that churn is likely to repeat this time as well. The question is how long it takes and how deep is the interim pain inflicted on the workforce before the transition is completed.

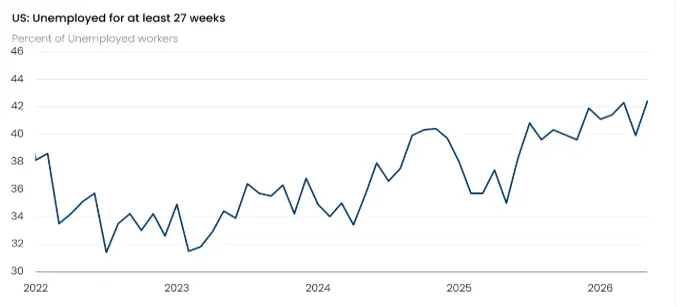

Simply put, the headlines of the jobs report – the blow-out increase in payrolls and the persistent low unemployment rate – paint a strong picture of the job market. Under the hood, however, an array of discrepancies describes more weakness than strength. Along with the lengthening time of unemployment for job seekers, existing workers are receiving slower wage gains. The annual increase in average hourly earnings slipped to 3.4 percent in May from 3.6 percent the previous month and are up by an annual rate of 2.8 percent over the past three months. A year ago, worker pay was increasing at a heftier 4 percent. Despite the strong payroll increase and low unemployment rate, worker bargaining power is not strengthening. Nor is their purchasing power. The consumer price report for May is not out till next week, but if the April year-over-year 3.8 percent increase holds, real earnings will once again have declined.

That’s bad news for workers, but good news for the Federal Reserve as it confirms that wages are not a source of inflationary pressures, which continue to stem mainly from higher energy prices and supply disruptions tied to the Mideast conflict. There is no reason to believe that the knock-on effects from that conflict will feed on themselves and fuel a sustained increase in inflation. Hence, the increasing odds, priced into the financial markets, that the Fed will increase interest rates this year are overblown in our view. But in light of the ongoing strength in job creation and uncertainty over when the oil spigot will reopen, prompting a retreat in energy prices, there is little pressure on the Fed to cut rates. From our lens, the Fed will keep rates on hold at least through the end of the year, when presumably a more languid geopolitical landscape will emerge and leave the Fed in a better position to assess the balance of risks facing the economy.