Kevin Warsh was sworn in as the new Federal Reserve Chairman on Friday, ending the eight-year leadership of Jerome Powell. Mr. Powell will not be leaving the Fed, as is customary, but will be moving down the table as a governor until he deems conditions are right for a departure. We expect the transition to be uneventful, as Powell is committed to a smoothly functioning central bank and respects – and will do nothing – to disrupt the authority of the Chair. Indeed, Warsh might face more obstacles from the White House than from Powell in coming months, if not years. After all, the president installed Warsh with direct marching orders: Cut rates as soon as possible, if not earlier.

For a good while after Trump announced Warsh as his pick on January 20, that seemed like a distinct possibility. Job growth slowed around the turn of the year, consumers were feeling the pain from tariff-induced price increases, and most Fed officials thought that inflation would retreat after the tariff-effect waned. At the March policy setting meeting, the Fed penciled in two rate cuts this year and more in 2027. But that was then. Since the U.S. war with Iran erupted, the economic landscape has changed dramatically. Instead of falling off a cliff, the labor market regained its footing, generating far more jobs than expected. Consumers are still spending, led by high-net-worth households with turbocharged asset gains from the stock market, and AI investment outlays are adding a powerful boost to growth. Most important, inflation has not only remained stubbornly high, it’s accelerating thanks mainly to surging energy costs.

As the notable economist John Maynard Keynes opined in the last century… “When the facts change, I change my mind. What do you do sir?” That sentiment has clearly infiltrated the Fed’s thinking in recent months, and the odds of a rate cut this year have fallen precipitously. Indeed, the financial markets are pricing in greater odds of a rate increase than a cut before the end of the year, something that clearly will not sit well with the president. That shifting mindset was starkly revealed in the minutes of the last policy meeting in April released this week. The gist of the discussions around the table was that the bar for rate cuts in the foreseeable future is considerably high. The Mideast conflict would have to end soon, inflation would need to start convincingly moving back towards the 2 percent target, which it has consistently exceeded for five years, and cracks in the labor market would need to become far more visible that it is now.

None of those conditions is on the near-term radar. Remarkably, despite the Fed’s shifting stance away from rate cuts, the stock market engine keeps on chugging along. Friday’s gain punctuated the longest weekly winning streak for the S&P 500 since 2023, something that will keep a fire under spending by upper-income households. For the lower-income cohort that has little in the way of stocks and a lot in the way of debt, the embers are getting cooler. Usually rising stock prices accompany falling interest rates, as the latter portends stronger and broader growth going forward. This time, however, that relationship has fallen by the wayside.

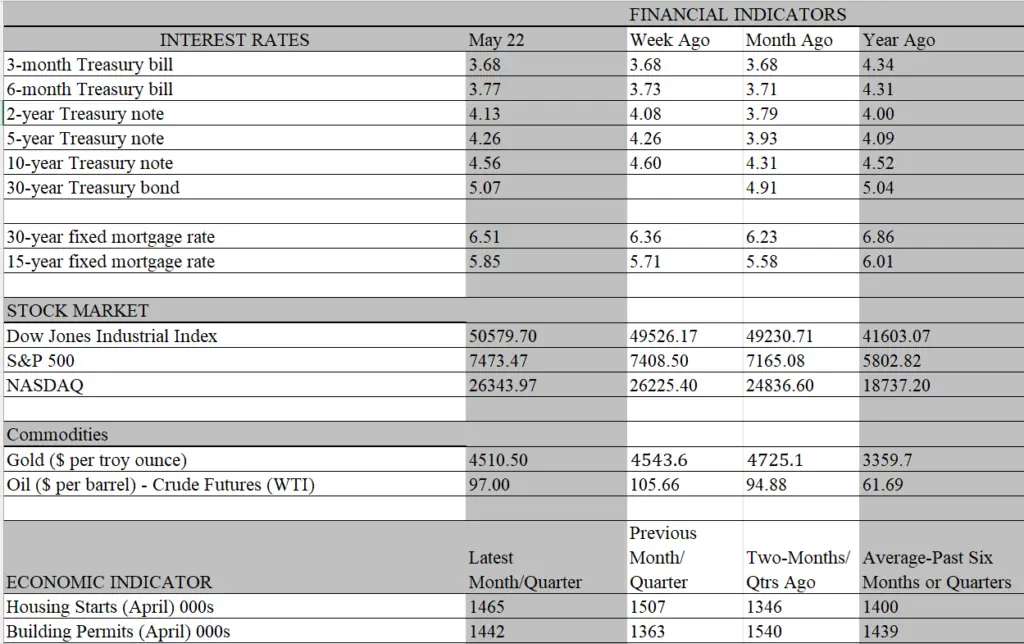

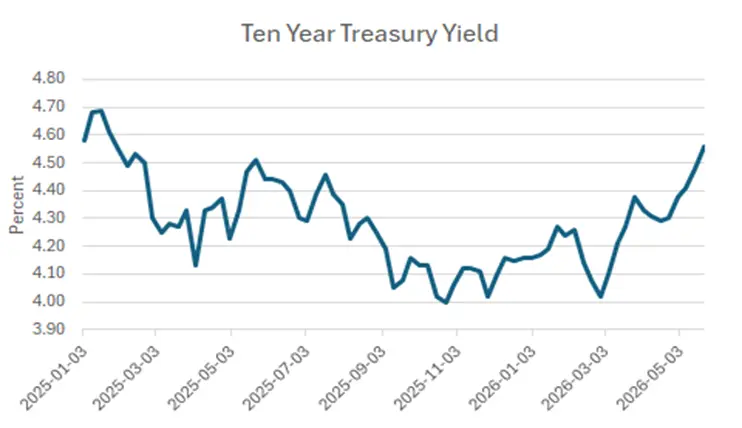

While the Fed has kept its short-term policy rate unchanged this year, market yields have moved up sharply since the outbreak of Mideast hostilities on February 28. The bellwether 10-year Treasury yield topped 4.5 percent this week for the first time since the Liberation Day tariff announcements last spring and yields down the maturity ladder have also staged big increases. Hence, budget-strapped borrowers are seeing their debt-servicing charges increase, adding another layer of expense to the rising cost of groceries and other essentials. The hurdle for first time home buyers is also moving higher as the mortgage rate, which not too long ago fell below 6 percent, is now firmly above that threshold, settling at 6.51 percent this week.

Part of the reason for the yield increase stems from the shift in expected Fed policy, since longer-term rates capture investor expectations of how short-term rates will evolve over time. But it also reflects longer-term inflation expectations, as higher prices erode the purchasing power of a fixed interest rate. Hence, the higher is expected inflation, the higher is the current rate demanded by investors to compensate for that loss of future purchasing power. Until recently, the Fed took comfort in the fact that long-term inflation expectations remained anchored, consistent with the widely held notion that once the Mideast conflict ends, inflation would retreat.

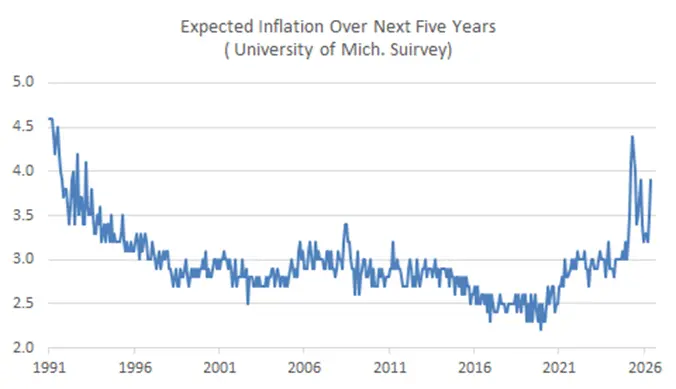

That notion is not so widely accepted now. According to the latest household survey released by the University of Michigan on Friday, long-term inflation expectations shot up to 3.9 percent in May from 3.5 percent in April and 3.2 percent in March. Except for the peak following the Liberation Day tariffs last year, you would have to go back more than thirty years to find a higher level of inflation expectations. True, it is a mistake to make too much out of a one- or two-month movement in the data. The post Liberation Day spike quickly reversed when Trump backtracked on some of the more extreme tariff threats. The Fed prefers to look through temporary shocks in its rate-setting policy decisions.

But there is more to worry about now. As noted, inflation has remained elevated for five years – and still heading in the wrong direction; high oil prices will linger even if the Mideast crisis ends soon, as it takes time to rev up production and reopen shuttered oil wells; and the oil price spike is already having second-round effects, boosting airfares, freight charges, fertilizer, groceries and bleeding into myriad other prices. We suspect that the sharp increase in inflation expectations overstates what inflation will turn out to be over the longer run. Worker bargaining power has weakened, undercutting the threat of rising labor costs that would feed inflation. Consumer resistance to high prices is growing and productivity gains should enable businesses to hold the line on prices without damaging the bottom line.

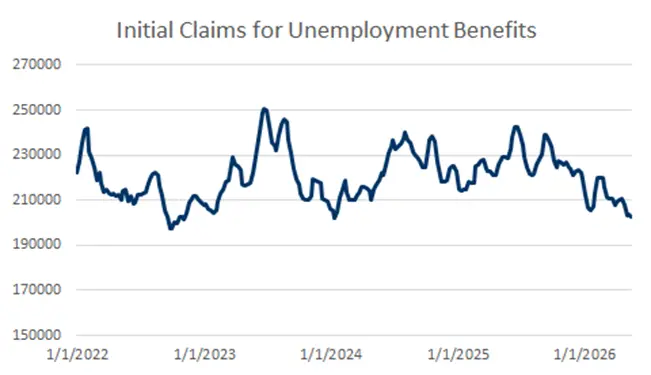

That said, the increase in inflation expectations is another reason for the Fed not to cut rates in the foreseeable future, and we suspect it will keep its finger off the trigger at least through the rest of this year. Things could change if the labor market suddenly turns south, heightening recession risks. But by all accounts, employers are hanging on to their workers, despite some high-profile layoffs related to AI. The historically low unemployment rate, at 4.3 percent, indicates that virtually anyone that wants a job has one, and state employment offices report short lines of people filing for jobless benefits. This is not a job market that looks poised to crack and require immediate help from the Fed. However, the longer the Mideast war continues, the greater will be the toll it takes on household incomes, as prices are already outpacing wage increases. Fed watchers will at some point pay more attention to geopolitical events than to economic data in forming expectations of Fed policy.