It was a momentous week on several fronts. The economic calendar was chock full of data, a new chair of the Federal Reserve was confirmed, and the U.S. President flew to China for a high-stakes summit with President Xi Jinping. While not on the agenda, the last item carries resonance for monetary policy, if only because it briefly denied the president a close-up microphone to demand an immediate rate cut from Kevin Warsh, his pick for the job. Not that it would matter as Warsh is most likely aware of the unfavorable landscape for a rate cut — a prospect that turned even grimmer this week.

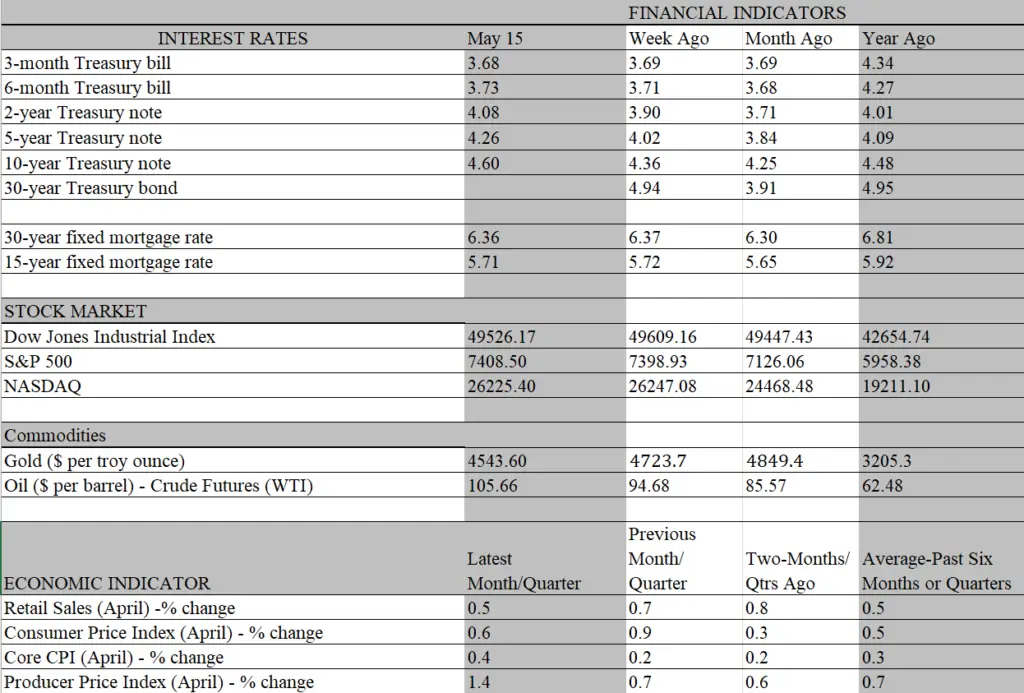

The most notable headwind pummeling the case for a rate cut, of course, is fresh data this week showing a further escalation of inflation. The 3.8 percent year-over-year increase in the headline CPI for April was not a surprise as it was spot-on with the consensus forecast. But the acceleration from 3.3 percent in March was nonetheless jolting, even though it was primarily driven by the well-telegraphed surge in gas prices. Nor did the slower 2.8 percent rise in the nonenergy (and food) core index provide much comfort to Warsh, as it was punctuated by a 0.4 percent monthly increase in April, the steepest for a month since December 2024. Hence, signs that the war-induced energy price spike is bleeding into broader inflation are proliferating, which could stoke inflationary expectations if confidence in the Fed’s inflation-fighting commitment falters.

The bond vigilantes are already making their voices heard. The 10-year Treasury yield topped 4.5 percent this week, passing the peak level reached in the aftermath of Liberation Day tariff announcements last April. The off-the-cuff remark by President Trump suggesting that we don’t need the Strait of Hormuz to open at all did little to assuage fears that oil prices will keep on climbing. Nor does the inflation pipeline offer much hope for near-term relief as the producer price index staged a nosebleed 6 percent year-over-year increase in April, the strongest in more than three years. Given this backdrop, the next policy meeting on June 16-17, the first helmed by the new chair, is almost certain to keep rates at their current level. It will be interesting to see how Warsh communicates that decision in his post-meeting press conference without drawing a backlash from the president.

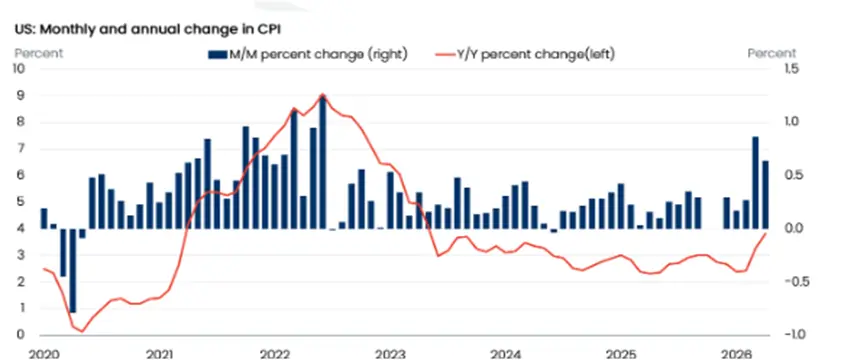

Complicating matters even more is that elevated inflation is not yet deterring consumer spending, diluting the best case for lowering rates. Clearly, many car owners, particularly among lower- and middle-income drivers, are sacrificing other purchases to fill up at the pump. But overall sales at retailers are holding firm as cash registers rang up a respectable 0.5 percent increase in receipts in April. And while the price-driven surge at gas stations had a heavy influence, accounting for the highest share of total sales since late 2023, the core group of sales that feeds directly into personal consumption in the GDP accounts, also rose by a lofty 0.5 percent. Following the upward revisions to previous months, real consumer spending is on track for a sturdy 2 percent growth rate in the second quarter, which would outpace each of the previous two quarters.

The resilience of consumers in the face of some formidable headwinds has been a stand-out feature of the economy since the pandemic, thanks to a recognizable list of catalysts. They include a burst of wage growth amid labor shortages coming out of the recession; copious pandemic era fiscal stimulus; a powerful wealth effect from surging stocks and until recently, house prices and, finally, ample tax refunds that more than offset higher gas prices so far this year. All but possibly the wealth effect have either faded or are on the cusp of doing so. Meanwhile, with no resolution to the Mideast conflict in sight, it’s unclear when the oil price climb will end and relieve the biggest source of inflationary pressures. That confluence of receding financial support and stubborn inflation represents the major threat to sustained consumer resistance. It also highlights a conundrum facing the Fed.

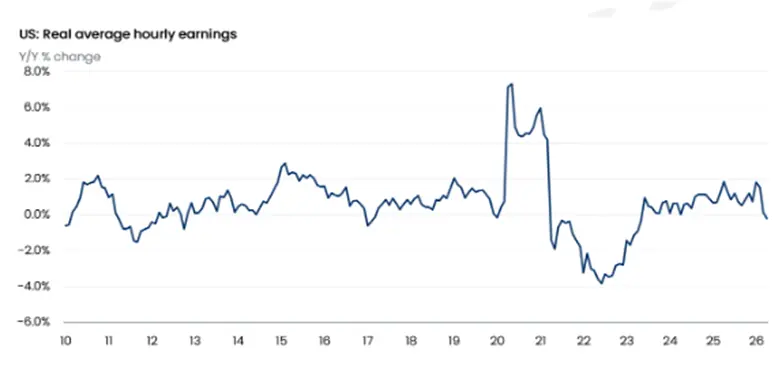

For the first time in three years, wage growth failed to keep up with inflation, as real average hourly earnings slipped 0.2 percent from a year earlier in April. On the surface, the decline in worker purchasing power does not bode well for consumer spending, as the majority of consumers rely mostly on labor income to finance outlays. Wealth gains garnered by upper-income households have accounted for most of the heavy lifting behind spending this year, but that continued support is never a sure thing amid a fickle stock market. Conversely, the odds that real incomes will continue to slip over at least the next few months are high.

That said, the job market, while sporting cracks, is also holding up better than expected. Companies are hanging on to workers, the pool of available labor is shrinking, and the unemployment rate has barely budged from its historically low level of just above 4 percent. With so little slack in the labor market, it is fair to wonder if workers will soon be in a stronger bargaining position to restore lost purchasing power, demanding larger wage increases to catch up with inflation. That, in turn, could set the stage for the dreaded wage-price spiral feeding on itself, heightening pressure on the Fed to raise interest rates.

While unlikely, that is more than a nontrivial prospect given the structural changes and, more important, unexpected currents that have upended the job market in recent years. The endgame from AI, demographic trends and immigration policies is far from settled, as these forces are still very much playing out. From our lens, a more benign outcome is on the near-term horizon. A resilient, but fragile job market, keeps a floor under wages while post war inflation recedes, allowing workers to regain lost purchasing power. That, in turn, sets in motion a more balanced growth/inflation outlook for the economy, allowing the Fed to resume moving its policy rate towards a lower neutral level. But the conditions for that move will probably not be in place until the end of the year.