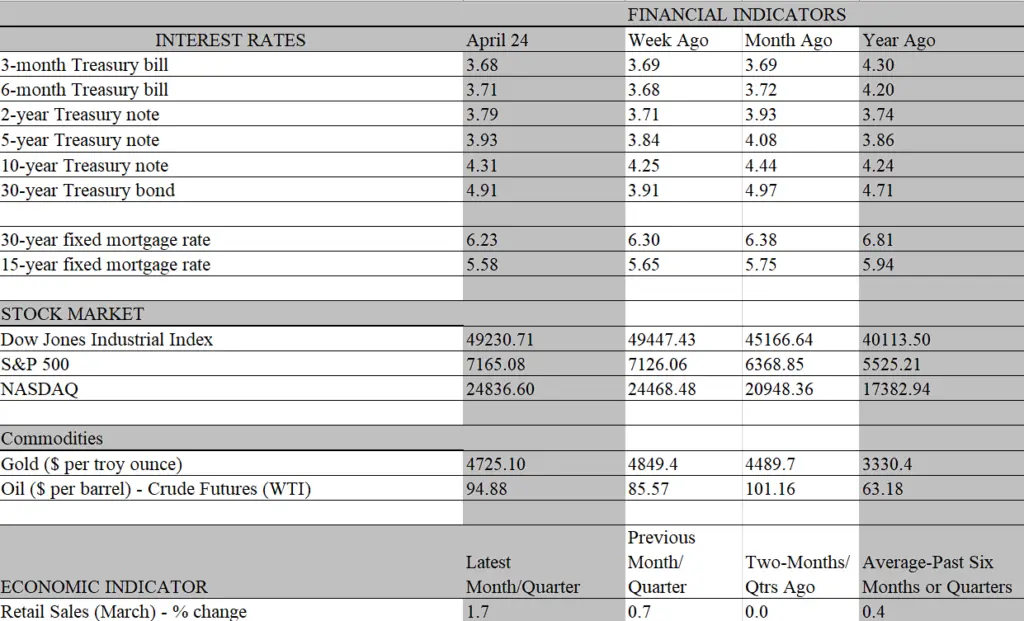

The week began with more questions than answers and ended much the same way. Topping the list of unresolved issues is the Mideast conflict, which continues to have no end in sight, despite on – again, off – again negotiations. That being the case, the question of how much damage the economy will suffer from one of the greatest disruptions in the energy markets in modern history remains open to debate. On the policy front, the question is how will the Mideast conflict influence the Fed’s rate-setting decisions at upcoming meetings. The oil-induced price hike is clearly giving the near-term inflation outlook a significant boost, portending the delay of expected rate cuts. But it is also taking a growth dampening bite out of incomes and purchasing power, strengthening the case of the doves for rate cuts sooner rather than later.

With a new Fed chair, Kevin Warsh, poised to take over the helm, the question is whether he will immediately push for rate cuts aligning with President Trump’s wishes. The Senate confirmation hearing this week did little to clarify that issue. Senator Warren harped on Trump’s boast that rates will fall when “my man” takes over the helm. But Warsh noted that the economy is at full employment at the hearing, and he was firmly against the steep rate cuts taken to counter the Great Recession during his earlier stint as a Fed governor. He also criticized the Fed for not raising rates soon enough when inflation took off in 2022. Like Supreme Court justices, the president’s choice of a Fed chair does not always abide by his wishes, including the outgoing chair Powell who was appointed by Trump.

The odds that Warsh will be confirmed in time for the June 16-17 meeting increased greatly on Friday, as U.S. Attorney Jeanine Pirro announced she was dropping the investigation into Powell, clearing the way for the Senate to confirm Warsh. That answers one outstanding question heading into the week but leaves open the question of whether Powell will stay on as Governor, which still has more than two years to run. Powell indicated he will stay on until the probe is dropped with “finality”. However, he may take umbrage with Pirro’s follow-up statement “Note well, however, that I will not hesitate to restart a criminal investigation should the facts warrant doing so”. No doubt, some reporters will ask Powell at the post-meeting press conference next week whether that statement will influence his decision to stay on. If he confirms leaving on May 15, don’t be surprised if he receives a standing ovation at the conclusion of his final press conference, rivaling the response to the announced first pick of Fernando Mendoza at this week’s NFL draft.

Clearly, the post-meeting press conference at next week’s FOMC meeting will draw more interest than the outcome of the meeting itself, when rates are expected to remain unchanged. We suspect that at the mid-June meeting, the new chair would have a tough time persuading his colleagues to cut rates, whether or not Powell is still onboard, if current trends persist. There will be two more releases tracking inflation, which will still be under pressure from oil-induced price increases. Even if the war ends and crude prices retreat, the lingering effects of the historic disruption of the oil markets will still be filtering through to retail prices. If that seeps into long-term inflation expectations, which remain anchored so far, the Fed’s resolve to stay on the sidelines would stiffen.

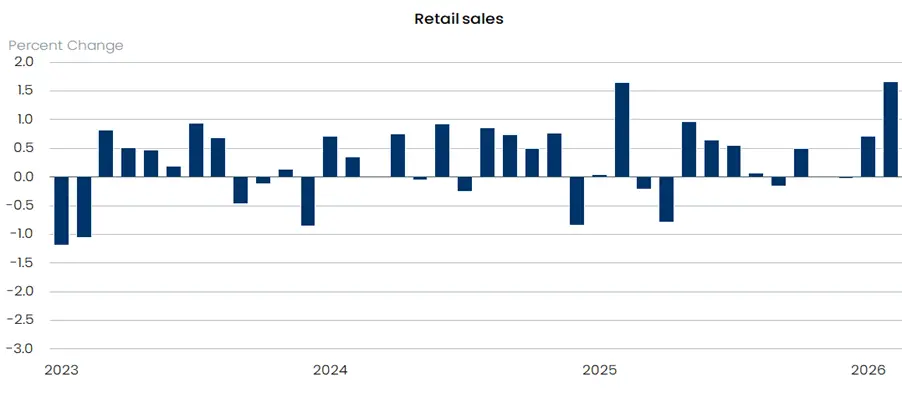

What’s more, there is little sign that the hit to incomes from higher energy costs is putting much of a dent on consumer spending. Retail sales staged a bigger jump in March than expected and while an outsized chunk of the increase reflected price-driven gas-station sales, virtually all other sales categories increased as well. With a faltering job market and slowing income growth, the shopping binge did not arise from organic forces that would sustain this pace of spending. Rather, consumers received a big increase in tax refunds over last year, which quickly found their way into the spending stream. Lower income households likely propelled the gain as they tend to file earlier than wealthier taxpayers, and this cohort spends every penny of additional income.

With most of the refunds disbursed, the spending boost from that source will fade. Some consumer relapse should be expected, but it will be cushioned by middle- and upper-income households whose spending is heavily linked to the wealth gains derived from asset holdings. Despite the fact markets loathe uncertainty – and there is still plenty surrounding the Mideast conflict – they have adopted a “what me worry” attitude throughout most of the war. Stock prices are hitting new highs and market yields have risen, but not to crippling levels. As of Friday, the bellwether 10-year Treasury yield is a slim 10 basis points higher than at the start of the year. Simply put, while Main Street is struggling with stagnant job growth, slowing wage gains and a historic slump in household sentiment, corporate earnings continue to forge higher and support stock prices – keeping a positive wealth effect intact.

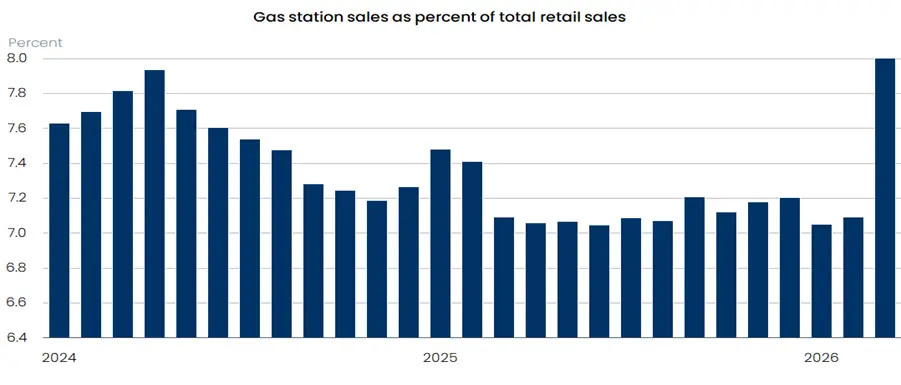

But the sooner the war ends, and oil prices retreat, the greater the odds that consumers — the economy’s main growth driver – will keep their wallets open and set the stage for stronger growth over the second half of the year. The headline spike in retail sales last month was heavily influenced by higher prices at the pump; the more lower – income households spend to fill up the tank, the less they have for everything else. Last month, gas stations accounted for 8 percent of total retail sales, up 1 percent from February. That share has been exceeded before, most recently following Russia’s invasion of Ukraine in 2022. But the 1 percent month over month increase was the sharpest at least since 1992, and the sticker shock from that budget-guzzling surge may send a broad swath of consumers into hibernation until it wears off.

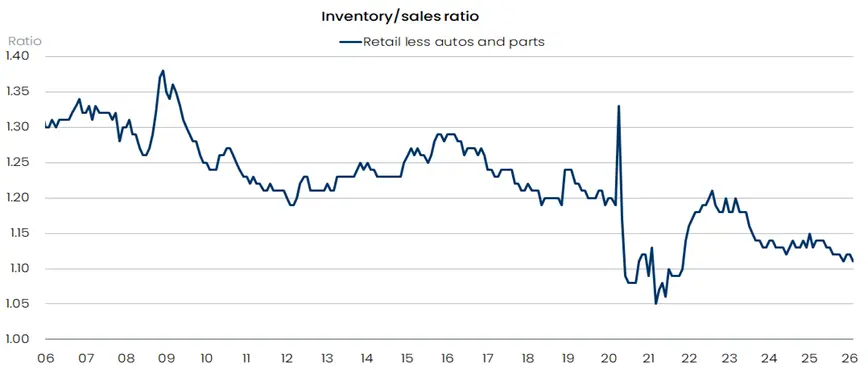

That, of course, would enhance the prospect of a rate cut sooner than later, as the Fed responds to the growing risk of a recession. Assuming the oil price influence wanes, the decision would clearly be easier to make. However, we note that it is not just oil propping up inflation as many retailers are short of merchandise and may have to raise prices to meet demand. Except for the extreme product shortages during the pandemic, the inventory/sales ratios for nonauto retailers has never been lower than it was in February.

It’s unclear whether this was a voluntary drawdown, reflecting caution over future sales prospects amid a highly uncertain landscape, or an involuntary reduction due to stronger than expected demand and/or tariff-related supply constraints. If the former and retailers are caught short of goods should demand exceed expectations, the pressure to raise prices would intensify. But if it was an involuntary reduction, the main effect would be to stoke growth, as restocking efforts results in increased inventory spending. Unfortunately, neither scenario points to easing inflationary pressures.