It will take time for the dust to settle, but Friday’s employment report clearly kicked up a sandstorm, prompting markets, pundits and oddsmakers to reassess the economic landscape and the policy response. Predictably, the surprisingly downbeat news on the jobs front ignited a dramatic knee jerk reaction, as it undercut widespread notions of the economy’s resilience. Its ability to withstand a barrage of headwinds, including geopolitical tensions, trade uncertainty, a draconian immigration policy and a looming game-changing mid-term election, has given it a Teflon-like sheen of invincibility. But the jobs report is always the dominant headline grabber among economic indicators, and the February report did not disappoint. In the immediate aftermath of its release, the VIX volatility index – a so-called fear gauge of investor sentiment – shot up to the highest level since President Trump’s Liberation Day tariff announcements last April.

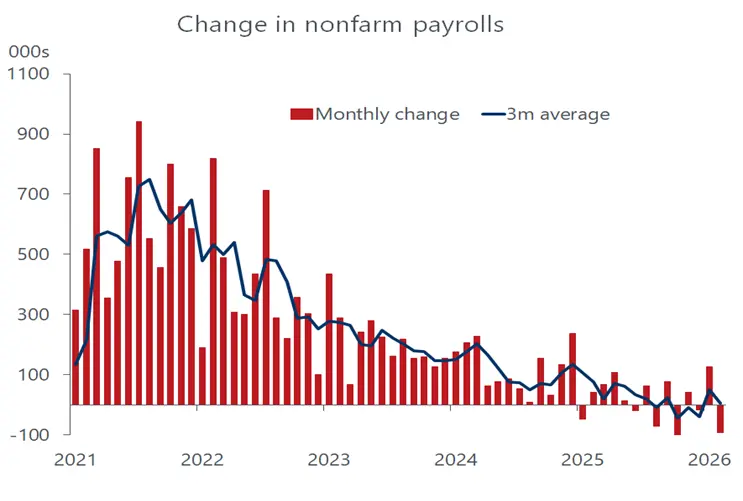

It’s hard to say when the dust will settle and fears subside given that the latest catalyst reinforcing market jitters – the war with Iran – is still in full swing. What’s more, the data for the downbeat February employment report were collected before tensions with Iran morphed into an outright war, sending oil prices skyrocketing and bringing stagflation concerns to the forefront. That said, we believe that the unexpected 92 thousand loss of jobs in February and the 0.1 percent uptick in the unemployment rate to 4.4 percent exaggerate the weakness in labor conditions, albeit it confirms the evolving fragility that accompanies a persistent “low hiring, low firing” condition in effect over the past year. After revisions to previous months’ data and smoothing out noisy movements for a single month, that condition still seems very much intact.

The revisions wiped out 69 thousand jobs from previous estimates of December and January payrolls, which adds to the sting of the February losses. However, even with those downgrades nonfarm payrolls staged a hefty 126 thousand gain in January and an even more impressive 146 thousand increase in the private sector. Aside from the usual noise in monthly reports derived from imperfect surveys, unpredictable weather and strikes can also play havoc with the data, as they did in February. Smoothing the data over three months paints a less dire picture, with private payrolls growing by an average of 18 thousand over the period. That’s close to our estimate of how many jobs are needed to keep the unemployment rate from rising, given the drag on the supply of available labor from slowing immigration and an aging population.

To be sure, the fact that just about every major sector shed jobs in February indicates that the malaise is spreading. But that was not the case in January, when most industries added jobs, although they were dwarfed by ongoing robust additions to healthcare payrolls. A nurses’ strike in California causee the turnaround last month, and we expect a sturdy rebound in healthcare jobs in March. As for most of the other sectors, the biggest loser last month was in leisure and hospitality, which saw a 27 thousand drop in payrolls, but that probably reflects frigid weather and snowstorms during the month. We suspect that attrition accounted for the modest declines in most other sectors, as companies are managing headcount more conservatively amid a highly uncertain backdrop and, to some extent, AI displacement.

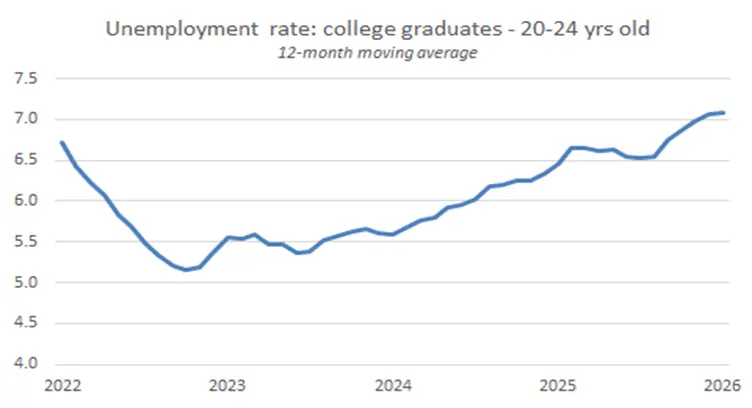

Regarding the latter, the continued surge in productivity in last year’s fourth quarter amid slowing job growth is amplifying the debate as to what extent companies are using AI to replace workers. The jury is still out on that issue; but the adoption rate of AI technology is still in its early stages and its current impact on jobs is probably modest at best. That said, it aligns with the “low hiring” part of the ledger as it concerns the struggles of young adults who spent their college years studying to get a leg up in the high-paying tech sector, where AI is gaining a stronger foothold. This cohort is accounting for an ever-growing share of job seekers on the unemployment lines. The Labor Department releases data on young college graduates with a one-month lag, but the trend through January confirms the upward climb in unemployment among recent college grads aged 20-24

As for the general population, the trend has also drifted higher from the cycle low of 3.4 percent last April, but at 4.4 percent the February unemployment rate is still historically low. Indeed, the broader unemployment rate, which includes part-time workers preferring full-time positions, ticked down to 7.9 percent from 8.1 percent in January and is below the 8 percent of a year earlier. Other broad gauges of labor conditions also depict more firmness than weakness. The employment/population ratio remains at a healthy level, as does the ratio for the prime-age population (the 25-54 age group). Importantly, workers are still getting decent pay raises. Average hourly earnings increased 0.4 percent last month and 3.8 percent over the past year. That’s solidly above the inflation rate, sustaining the purchasing power of households.

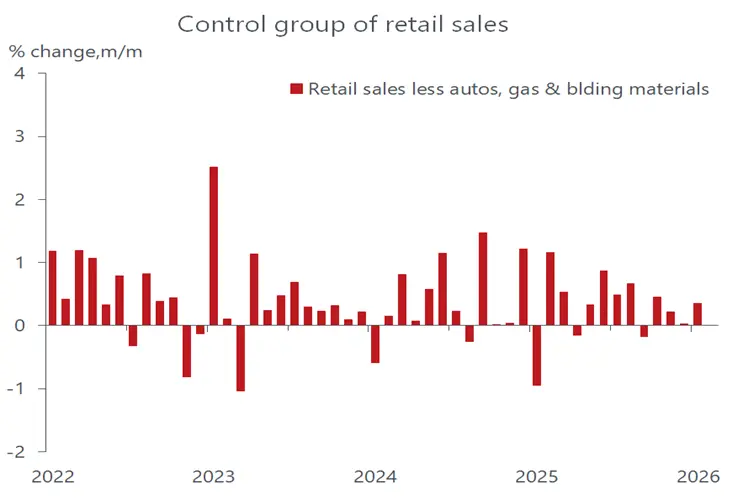

At first glance, it appears that households are preserving their purchasing power instead of spending it at the shopping malls. Along with the jobs report on Friday, data on retail sales for January was released. Overall, retailers suffered a 0.3 percent drop in revenues during the month. Since the setback occurred in a month of sturdy job growth, even after the downward revision, it’s reasonable to wonder how sales would fare in February amid heavy job losses. But like that jobs report, the January sales headline overstates the weakness in consumer spending. We know that auto sales, which account for about a third of total retail sales, rebounded in February from January’s slump. It’s also clear that inclement weather had a negative impact, cutting into sales at restaurants and bars as well as at sporting and other recreational events.

Another ironic drag came from declining sales at service stations, as prices at the pump were still falling in January. Obviously, that is no longer the case, as gas prices are surging amid the Middle East conflict that is driving crude prices to nosebleed levels, less than $10 below the $100/barrel level on Friday afternoon. One consolation is that consumers are spending less of their retail budgets on gasoline than any time since the pandemic. So there is a cushion before the cost of fueling up takes a painful bite out of income and sales. What’s more, the ding on overall consumption from January’s weak retail sales is less than the headline suggests, as the component that feed into GDP rose by 0.3 percent. While the gasoline “tax” will be a drag on consumer spending in the first quarter, it will be offset somewhat by the infusion of tax refunds into bank accounts, which are expected to be about 20 percent higher than last year.

We do not expect this week’s reports, headlined by the downbeat loss of jobs, to have an impact on the Fed’s decision to keep rates unchanged at its March 17-18 meeting. That said, the Middle East crisis and surge in oil prices will complicate the decision-making process even more if those conditions linger much longer. The Fed tends not to respond to sudden shocks, and the current one contains both an inflationary component (the surge in oil prices) and a demand destroying one (the surge in oil prices). Until a clearer picture of which one has more of an effect on the overall economy, the Fed will likely stay on the sidelines.